Luxembourg Real Estate 2020

Building blocks for success

Research enlightened by:

Wissam Mobayyed

Table of Contents:

Part one: Introduction

Part two: Everything gets bigger in Luxembourg

Part three: What does 2020 have in store?

- Office market

- Residential market

Part four: Trends and drivers for real estate’s evolving landscape

- Mobility within the country and cross-border countries

- International economic perspective for Luxembourg

- Demographic changes drive further demand

- Technology and sustainability will change the real estate landscape

- New sources of financing for real estate

Part One:

Introduction – The future for Luxembourg real estate should follow global trends

The Luxembourg real estate market – On and on goes the growth:

Luxembourg has seen outstanding development over the last decades, outperforming most other European countries. The country’s geographic and demographic characteristics are one of a kind. The combination of these factors has had an enormous impact on the real estate market. And this is set to continue.

The office and residential markets are the country’s main real estate drivers. Judging by the size of the country, their value is massive. Based on our predictions, both the office and residential markets are set to continue to grow until 2020, offering good investment opportunities.

Luxembourg has a lot going for it, especially in terms of security, and political and economic stability. And the future success of its real estate industry will largely depend on these distinctive features. Further development of the infrastructure will be instrumental for the country to remain attractive and at the same time address the changing needs of its residents (both nationals and foreigners). These challenges are at the top of the government’s agenda – many political measures are under way to maintain this privileged quality of life.

Another essential feature for real estate sector growth is the economic stability of the country. The last two years have been a turning point for Luxembourg – the country has taken major economic actions, showing its commitment to moving to enhanced cooperation in taxation and exchange of information. This will undoubtedly attract new arrivals, especially high-net-worth individuals. Taking this into account, GDP projections by both the Luxembourg government, and by supranational bodies such as the International Monetary Fund (IMF), are bullish. Other factors, including technological developments, increasing efforts to support sustainability and new sources of financing, are also expected to help drive the future of the Luxembourg real estate industry

An exciting time for the international real estate sector:

The international real estate sector will be at the center of rapid economic and social changes over the next five years. If well anticipated, real estate players can turn these new challenges into great opportunities.

Interest in real estate is already gaining momentum, as more and more investors allocate a significant share of their assets into real estate investments. Case in point: Standard & Poor proposed to break real estate out of financial assets and turn it into its own sector.

In our report, “Real Estate 2020: Building the future”, we projected that the worth of global institutional grade real estate will expand by more than 55% – from USD 29 trillion in 2012, to USD 45 trillion in 2020. Here are the coming challenges that we identified globally:

- Huge expansion in cities, with mixed results

- Unprecedented shifts in population driving changes in demand for real estate

- Emerging market growth ratchets up competition for assets

- ‘Sustainability’ transforms design of buildings and developments

- Technology disrupts real estate economics

- Real estate capital takes financial center stage

Our six predictions for 2020 and beyond

The real estate landscape in Luxembourg will change spectacularly in the coming years. Here, we highlight what we expect to be the main changes to come:

- The office and residential markets will grow by nearly 60% and 50% respectively over the period from 2012 to 2020. This growth is driven mainly by economic development and its resulting need for office space and an augmented workforce.

- The current volume of office space for rent will not be enough to meet demand. If the economy grows as expected, businesses will be squeezed for office space, and Luxembourg will experience a marked shortage of office properties.

- Mobility and infrastructure developments will be crucial to the country. With the projected increase of population and cross-border employee numbers by 2020, infrastructure needs will grow further, and efficient mobility solutions will have to be adopted over a tight timescale in order to keep pace with demands.

- The number of foreigners in Luxembourg City and its close neighborhood will keep on increasing, and the residential rental market will expand in this area. A growing number of Luxembourg nationals with lower income will move to surrounding regions within the country, or even move across the borders.

- More apartments than houses will be built, in order to best address the needs and budgets of households. The average number of persons by household has significantly decreased over the last decades, and this trend will continue with the arrival of new residents.

- New investors, both institutional and private, will come to Luxembourg. Pension funds and other institutional investors will show more interest in operating in the Luxembourg market, and high-net-worth individuals will keep on coming to Luxembourg.

Part Two:

Everything gets bigger in Luxembourg!

This is how we can say how fast the country has developed over the last decades. The growth of both the economy and population has been exponential compared with other EU countries

A fast-growing and competitive economy

– The workforce has almost doubled in 20 years whereas it increased by less than 20% in Europe

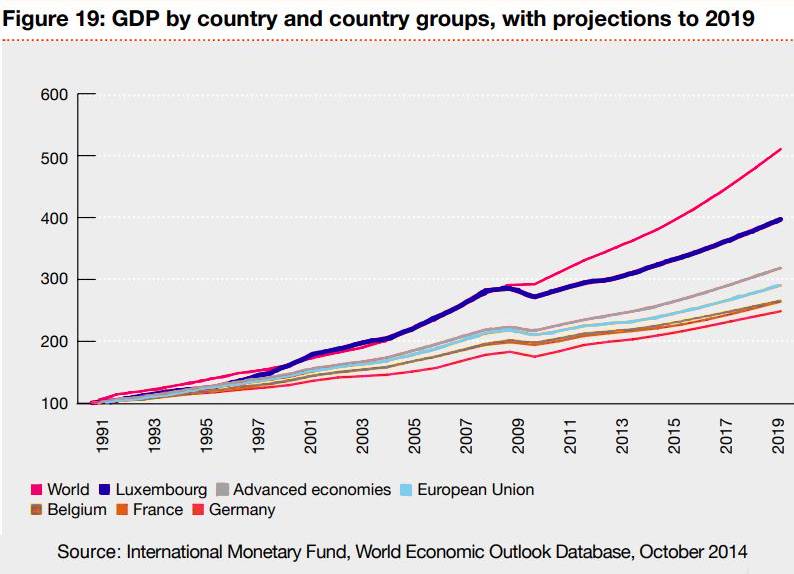

– The Luxembourg GDP has more than tripled from 1991 to 2014 while the Euro zone GDP doubled

On top of a stable political environment and sound public finances, Luxembourg’s main strength lies in its ability to adapt its economic strategies quickly . Before being a major financial marketplace, Luxembourg was initially an agricultural country. The steel industry then became the bedrock of the country’s economy. As that industry progressively declined, the government saw in financial services new sources of development. As the first EU country to adopt “UCITS” legislation into national law, in 1988, Luxembourg achieved a turning point in its history by becoming a major center for investment funds in Europe and in the world. The Grand Duchy made the most of its expertise in financial services, and quickly became a hub for banks and insurance companies. Nowadays, the financial sector is the strongest component of the Luxembourg economy – nevertheless the country is continuing to diversify its economy by investing in new industries, such as the logistics business and the Information and Communication Technologies (ICT) sector.

As a consequence, the size of the workforce has almost doubled in 20 years, whereas it increased by less than 20% in the European Union (EU) over the same period. In the same vein, Luxembourg’s GDP has more than tripled between 1991 and 2014, while Euro zone GDP merely doubled.

Luxembourg has also been able to attract major multinational groups, and has encouraged them in developing their activities in the country. The ranking of Luxembourg in international competitiveness surveys confirmed its attractiveness. In “The Global Competitiveness Report 2014 – 2015”, the World Economic Forum ranked Luxembourg 19th out of 144, up from 22nd in 2013. In the World Competitiveness Ranking, the country moved from 13th in 2013 to 11th in 2014. In most global surveys, Luxembourg position has moved up compared to their previous findings.

Furthermore, Luxembourg, along with Brussels and Strasbourg, is one of the European Union capitals. Several major EU institutions are headquartered in Luxembourg, such as the European Commission and Parliament, the Court of Justice, the Court of Auditors and the Investment Bank. Many European civil servants work in these institutions, contributing to the development of the country.

A growing and multicultural population

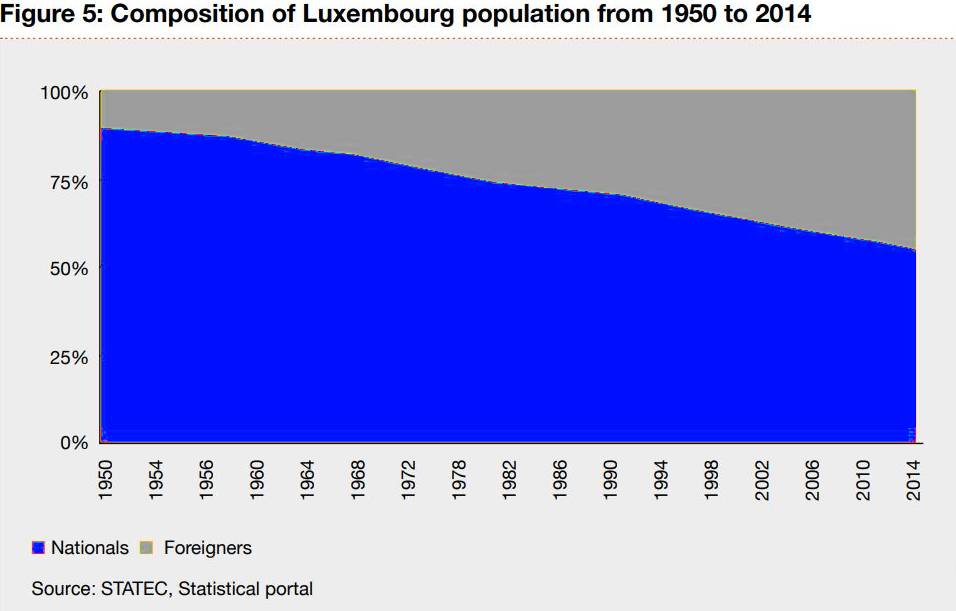

– The number of non-national residents is one of the highest in Europe, reaching a record high of 45% of the population

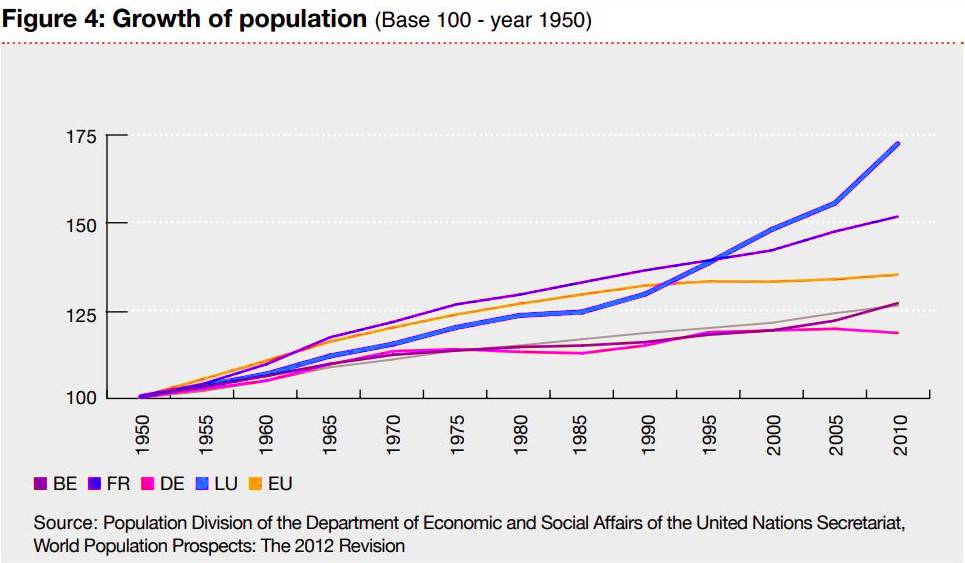

– The population grew by more than 70% from 1950 to 2010

The surge in population has been supported by the significant and ongoing arrival of foreigners to meet the needs of the growing economy. As a result, the number of non-national residents is one of the highest in Europe, now amounting to more than 45% of the population. Since 1977, the total number of foreigners living in Luxembourg has tripled5 . Most of these foreigners are coming from the EU, although the share of non-European arrivals is slowly but steadily increasing. This cosmopolitanism turns out to be an asset for the country, since most of the new comers are highly skilled workers. Case in point: The Global Talent Competitiveness Index 2014 ranked Luxembourg third globally in attracting talent.

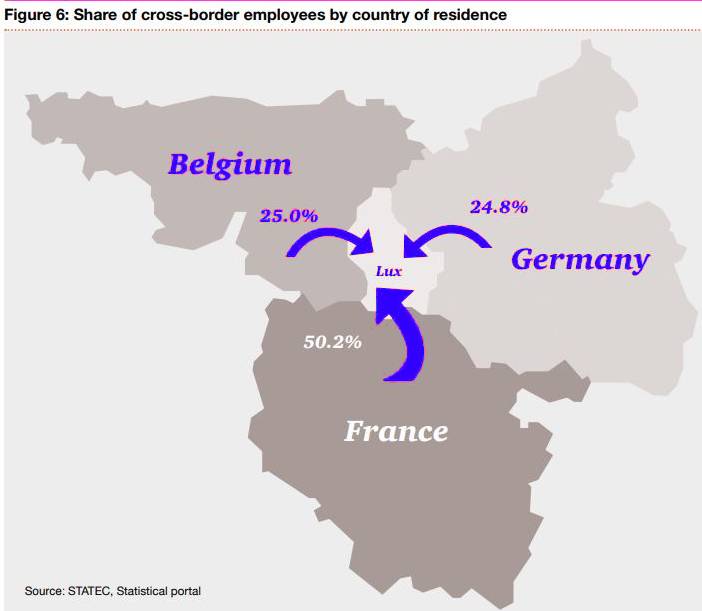

The highest level of cross-border workers in Europe…

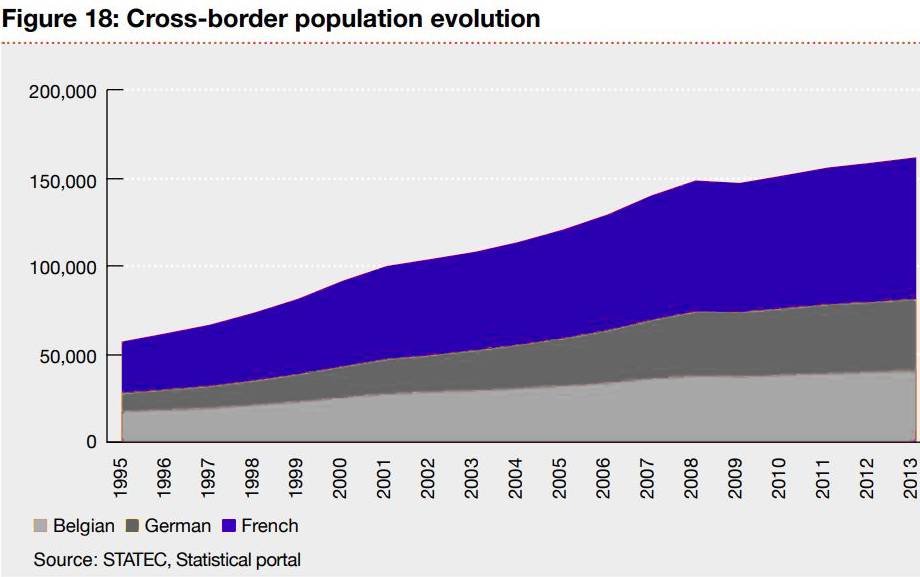

Luxembourg benefits from its central location, with proximity to Germany, Belgium and France. Cross-border workers account for more than 44% of the country’s labor force, contributing enormously to economic growth . The number of cross-border employees has tripled over the last 20 years . Currently, more than 160,000 cross-border workers commute to Luxembourg every day . The largest community of non-Luxembourg nationals commuting to Luxembourg appears to be the French, followed by Belgians and Germans. With the exception of very small countries such as Monaco and Liechtenstein, the level of cross-border workers is the highest in Europe.

…which results in traffic jam

– The number of cars registered in the country has increased by 35%

– The resident population has increased by 25%

– The cross-border population has grown by 75%

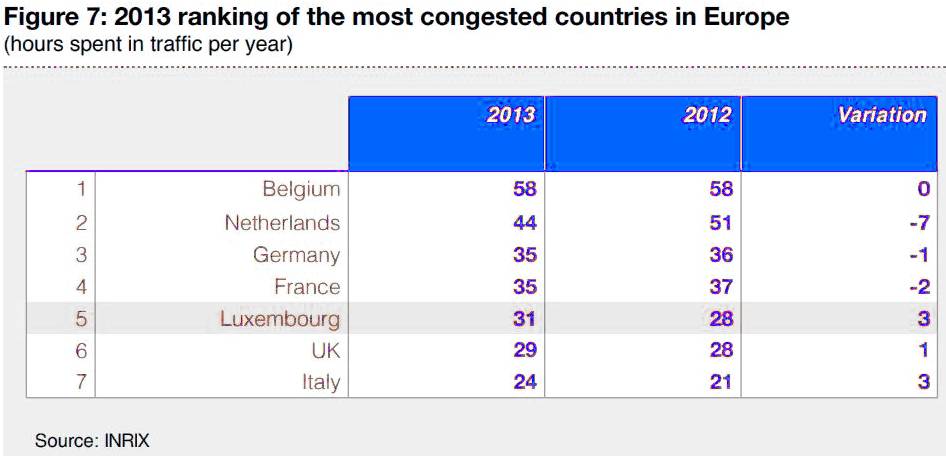

Mobility is at the top of the government agenda. With the growing number of cross-border workers, Luxembourg has become one of most congested countries in the world, ranking 9th on the INRIX scorecard in 2014, from 14th in 2010. Even despite substantial efforts having been made to encourage cross-border workers to use public transport, most still commute by car. The road network has remained virtually unchanged since 2000, whereas the number of cars registered in the country has increased by 35%, the resident population by 25%, and the cross-border worker population by 75%.

An expensive place to live

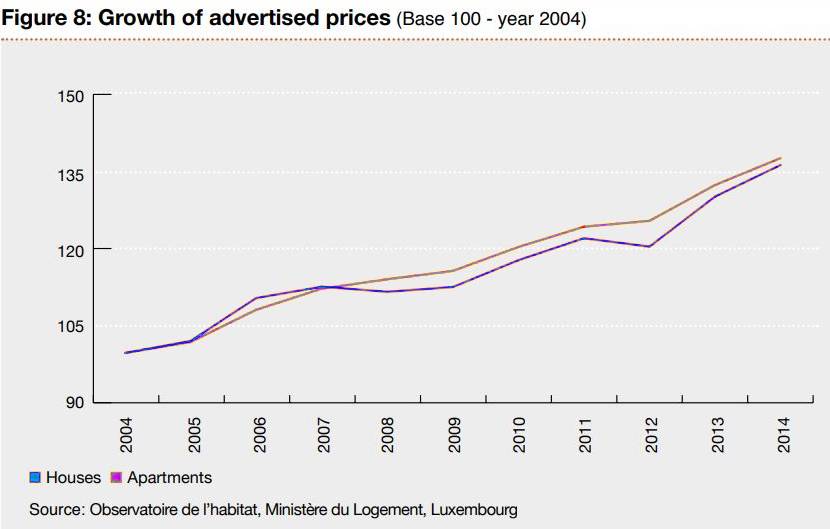

With such a surge in population, the demand for property has inevitably increased. The delivery of new dwellings for the last ten years has not met the needs of the growing population completely. As a consequence, the prices of both houses and apartments have risen by more than 35% since 2004.

In 2014, the average price for a house rose by 7% and that of an apartment by 2.9% compared to the previous year.

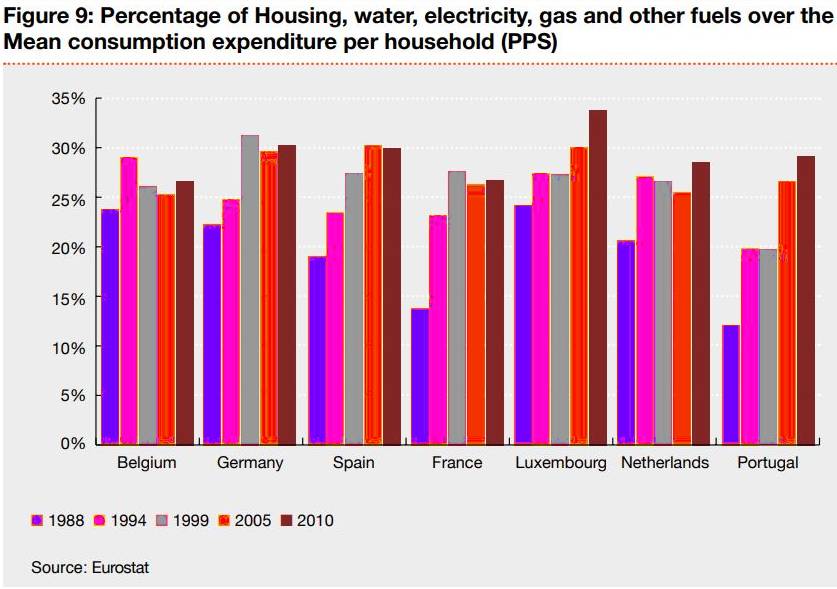

Living close to work is increasingly expensive. Luxembourg households spend over a third of their monthly expenses on housing, the highest rate in Europe.

Owner-occupiers are driving the residential market

– 85% of national residents own their house

– 50% of foreigners own their accommodation

Most Luxembourg residents own their primary residence. With nearly 71% of home ownership, Luxembourg is in line with the European average and Belgium (72%). However, there are significant discrepancies with neighboring countries, since home ownership stands at 64% in France and 53% in Germany. Such differences are even more significant within the country with about 85% of national residents owning their housing, against approximately 50% for foreigners.

A limited speculative office supply

The office market is highly correlated to the fast-growing economy of the country. As the need for new office spaces keeps on increasing, vacancy levels in Luxembourg’s central areas are low, and most office deliveries are pre-let, or pre-sold, before completion. Only a few investors are currently developing speculative office projects. However the risk of not finding tenants is quite limited, given that the demand for office space remains high.

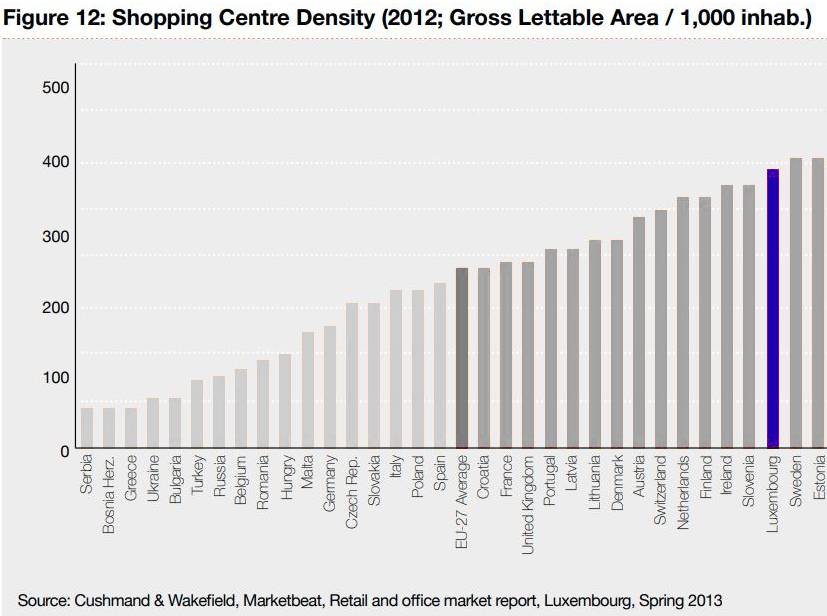

High shopping center density, serving the Greater Region

– The shopping center density per inhabitant in Luxembourg is one the highest in Europe

– The total surface taken up by major retail centers is predicted to surge by approximately 80,000 sqm by 2017, an increase of 16%

Shopping center density per inhabitant in Luxembourg is one of the highest in Europe. Nevertheless, the retail market still has some room for growth, since shops can increasingly tap into a large and growing base of customers coming from the Greater Region, as workers on week days and at weekends with their families.

With an estimated 500,000 sqm, shopping center area is already higher per head in Luxembourg than in almost all other EU countries. The total surface area of major retail centers is predicted to surge by approximately a further 80,000 sqm by 2017, an increase of 16%.

Part Three:

What does 2020 and 2021 have in store?

Although hit by the global financial crisis, both the office and residential markets are now again offering many interesting investment opportunities.

Our methodology

Based on information publicly available, we have determined the total value of the office and residential markets from 2004 to 2012, and developed our own projections for 2020. To do so, we factored in economic forecasts as published by the Luxembourg administration and other supranational bodies, and combined these with projections for population growth, other economic and demographic factors, and real estate brokers’ data.

1- Office Market

– By 2020, the office market will reach EUR 32 billion from EUR 23 billion in 2014, a 40% increase

– By 2020, Luxembourg will experience a marked shortage of office properties

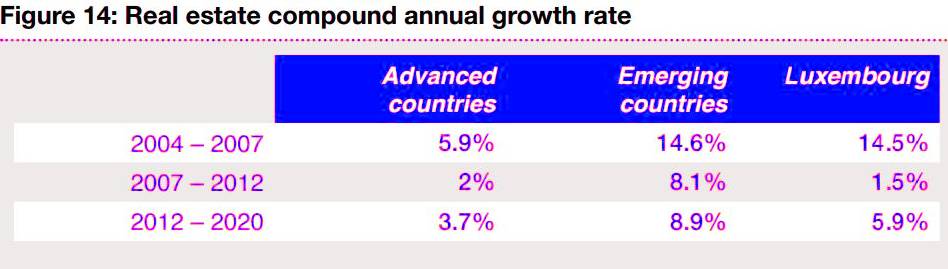

The total value of the office market in Luxembourg has been estimated to be around EUR 23 billion in 2014. Based on our projections, we expect this market to grow by a compound annual rate of 5.9% until 2020, reaching a total value of some EUR 32 billion.

Historically, with an annual increase of more than 14%, the value of the office market soared from 2004 to 2007. Hit by the global financial crisis, market growth slowed to 1.5% per year from 2007 to 2012.

How does Luxembourg real estate compare?

After a short-lived drop from 2007 to 2012, the Luxembourg property market’s growth has surged again, amidst a recovering economy. Despite being described as an advanced country, Luxembourg economic outlook is closer to the projected performance of many emerging countries.

Luxembourg combines the features of an advanced economy and the dynamism of an emerging country

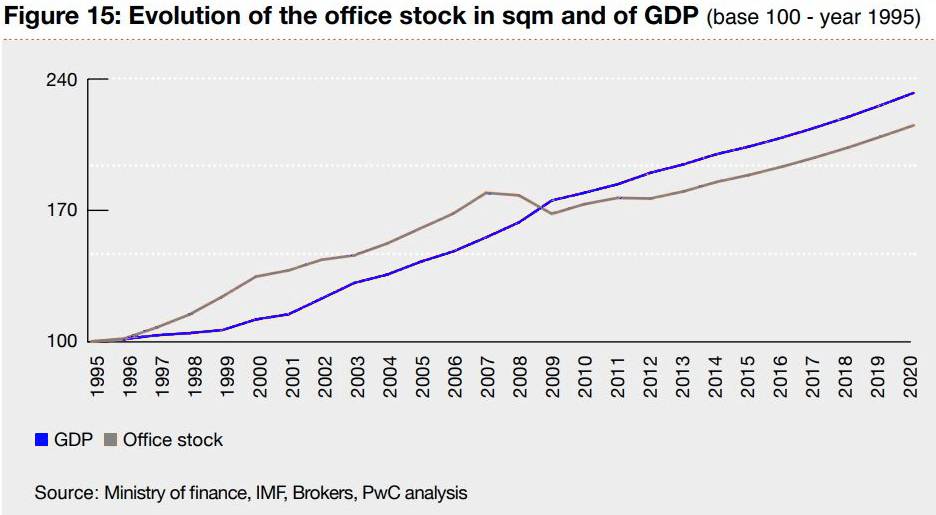

A crunch in office space as demand rises

With Luxembourg’s economic recovery, office leasing activity is now at its highest since 2012. As relatively little new office space is now being developed, we predict a coming supply crunch. The current volume of office space for rent will not be enough to meet demand, given that the vacancy rate stands at approximately 4% and may dip to 3% or below. As rising demand meets a lack of new development, office rents will automatically increase. In such a context, it is likely that the landlords will renegotiate more aggressively the rents of most prized properties.

On the one hand, this analysis should recognize some elements that could mitigate this predicted crunch in office space:

- changes in use of in-office space (open working areas are increasingly becoming the norm, and hence the number of sqm per employee decreases), and

- The increase of teleworking, which may be poised for growth with the further development of IT.

On the other hand, we have not taken account of any obsolescence within the current office stock, despite it being clear that the current tenants of old and non-eco-friendly properties are likely to move out, and that these properties will need to be refurbished in order to be re-let, or will have to be demolished.

These projected levels of demand and supply will lead to an increase in rent, and to further development of office properties in the suburbs, where there is currently lower rent and easier access. This is likely to attract institutional investors, who will see an opportunity for both regular cash inflow from rents and for capital appreciation.

2- Residential Market

– By 2020, the residential market will reach EUR 158 billion, from EUR 122 billion in 2014, a 30% increase

– VAT hike, from 3% to 17%, combined with mismatch of dwelling supply and high demand will keep prices high

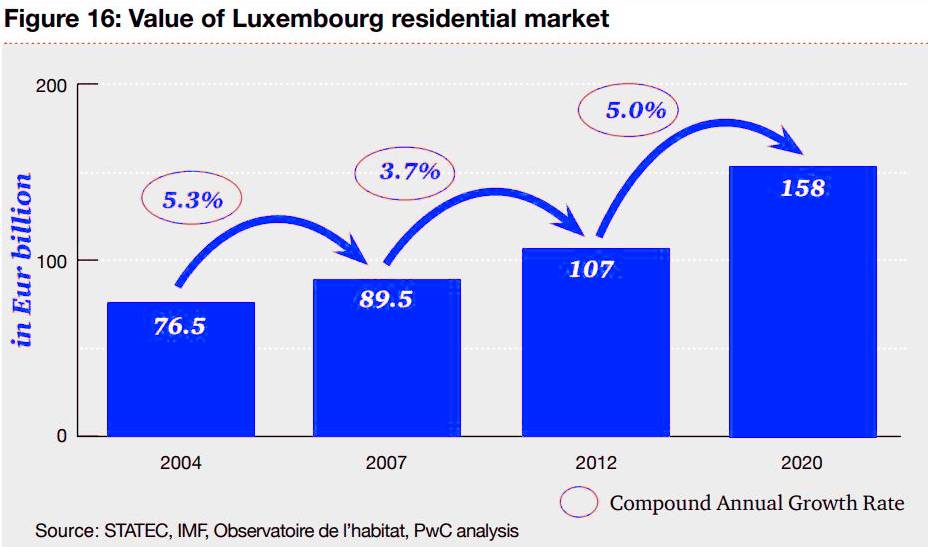

Within the Luxembourg real estate market, residential is by far the strongest. Its total value was over EUR 122 billion in 2014, and it will continue to grow at a compound annual rate of 5%, to nearly EUR 158 billion by 2020.

Since 2004, the residential market has grown steadily. The Luxembourg residential market was only moderately hit by the global economic crisis of 2008. Factors affecting the situation include:

- The population of Luxembourg has been increasing steadily since 2004.

- Demand has remained high, especially for apartments, which are more expensive per sqm than houses.

- Dwelling supply has generally not met the increase in demand.

- Building standards in Luxembourg are among the highest in Europe and the related costs of construction increased as well.

- Inflation has remained relatively high, with an average rate of 2.6% from 2004 to 2013.

Prices on the rise

With dwelling supply not fully addressing the increase in demand, which will now take years to match, prices have boomed. The 14 point increase in VAT, from 3% to 17%, will exacerbate this tendency. (On 1 January 2015, the VAT rate for construction and repair costs was raised to 17% for non-owner-occupied properties.) To counterbalance the higher investment cost, residential property investors will seek to raise rents. However, the increase in the price of property for sale and residential rents may not immediately move in line with the VAT rise.

The rental market is mainly concentrated in Luxembourg City and its neighboring areas. It primarily focuses on apartment letting. Residential property is mostly owned by private investors, as it is a long-held Luxembourgish habit to invest in bricks and mortar.

Part Four :

Trends and drivers for the evolving real estate landscape

We have identified the main trends and drivers which will change the real estate landscape considerably in the coming years. This overview could be a vital aid in planning for the medium-term future.

1- Mobility within the country and cross-border countries

Priced out: More and more people are moving to the suburbs

– Wider spaces are available

– Prices are more affordable

– Teleworking is spreading

Unaffordable rent and lack of offer push people away from the capital

Over the last 20 years, the total population of Luxembourg has increased by 40%, and the number of foreign residents has doubled. This significant surge in population has resulted in domestic migration. From 2005 to 2011, Luxembourg City experienced a negative net migration. More than 7,500 city inhabitants, i.e. almost 9% of the city population in 2005, turned their back on the capital. Soaring prices and lack of suitable properties have caused a surge in the number of people fleeing Luxembourg City to flock to the suburbs. In addition, Luxembourg City is moving slowly from being a residential ownership market to a rental market, encouraging people who want owner occupation of a property to move away from the city.

Working from home is becoming easier and easier, backed by IT solutions. And this adds to this domestic migration trend. But ultimately, despite all the above factors, the population of Luxembourg City increased by 30% over the period from 2005 to 2014. This growth has been mainly driven by the arrival of foreigners in the city.

Luxembourg City is mainly attracting foreigners

With most newcomers living near or around their workplace, this being most often located in Luxembourg City, demand for rental properties in the capital has soared, and rental prices have increased correspondingly

Global urbanization – Luxembourg makes no exception

Globally, millions of people are migrating from country to city. Through to 2020, this migration will continue. The cities will swell – and some entirely new ones will spring up. Luxembourg is no exception. Over the last decade, the urbanization of the country has been more marked than ever. From 2001 to 2014, 51% of the country’s population growth has been concentrated in the ten biggest communes, whereas it was only 19% over the period from 1970 to 2001.

This trend was even more marked over the last four years, as 55% of the total growth was in these top 10 communes from 2011 to 2014.

In Luxembourg, 19% of the population lives in the capital. But nearly 45% of the total population lives in the ten biggest communes in the country.

This trend will strengthen in the coming years, since the future delivery of apartments, being mainly located in the larger communes, will be higher than delivery of houses. In addition the government plans to rationalize the country’s landscape, preserving some areas from any construction, while intensifying urbanization in some other areas.

The need for cross-border employees will increase further

To meet the need for a growing workforce, Luxembourg companies increasingly have to tap into cross-border resources. As accommodation prices are high, the newcomers often live abroad, which raises the number of cross-border workers.

Based on our projections and the expected economic growth, the number of cross-border employees will grow by 25% over the next six years, up from approximately 160,000 in 2014 to more than 200,000 in 2020.

Outlook

Infrastructure development and mobility solutions are proving vital for urban success and a high quality of life in Luxembourg. Residential areas located close to work premises, and those connected to infrastructure and the public transportation network, will likely see their prices increase faster than residential properties in regions less well-connected. The rental market in Luxembourg City is expected to grow strongly, since it will remain the first choice for newcomers to Luxembourg

2- International economic perspective for Luxembourg

– Luxembourg’s GDP will grow by 23% from 2014 to 2019

– Luxembourg navigated the storm with a 5-year average growth of 2.5%, compared with 0.6% for the euro area and 1.6% for ‘AAA’ peers

A positive outlook towards 2020

The world is facing significant challenges: economically, politically and socially. Luxembourg can rely on its financial stability and triple A credit rating to face challenges looming on the horizon. The country has navigated the storm and performed well throughout the global financial crisis, with a five-year average growth of 2.5%, compared with 0.6% for the euro area.

With a growth forecast aligned with other advanced economies, and still ahead of the other main EU countries, Luxembourg’s economic future looks positive.

The financial sector will continue to be the main growth engine

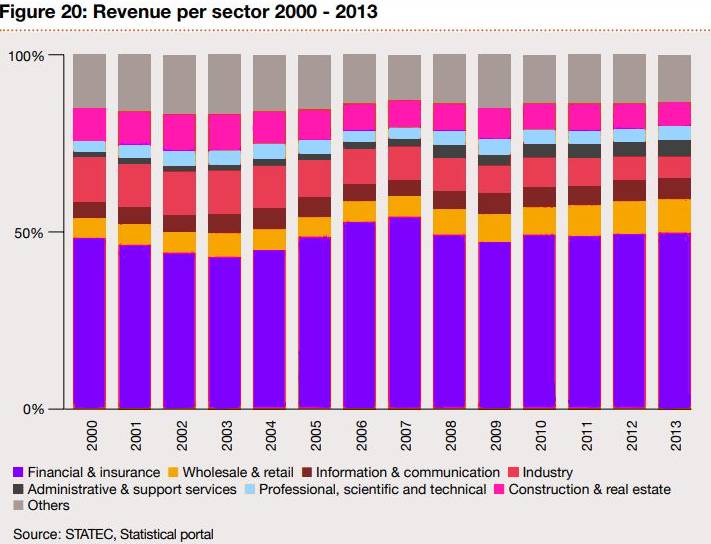

The financial services sector, including banking and insurance services represent approximately 50% of the total revenue for the country. In contrast, the share of the revenue attributable to heavy industry has halved since 2000.

The share for wholesale and retail business, and administrative and support services, increased from 7% in 2000 to 16% in 2013. In spite of a sustained level of activity, construction and real estate services saw its share decreasing to 7% in 2013.

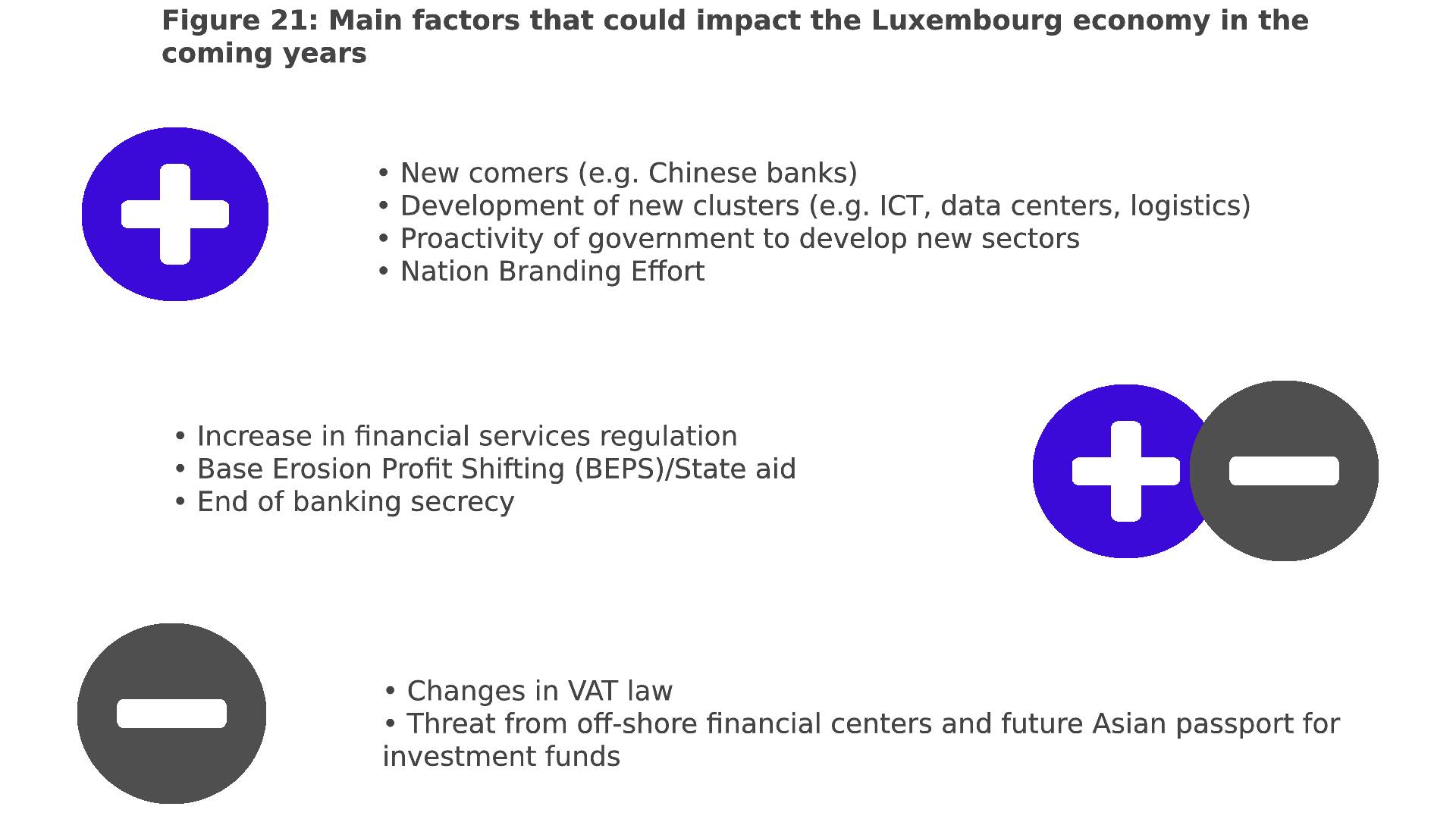

Even if some sectors have gone through important changes, the financial sector remains the main driver of the country’s economy. This also means that the national economy is more exposed to global financial shocks. But it also still constitutes an opportunity. Over the last three decades, Luxembourg has developed as an international financial center that is globally recognized for its high level of expertise. This financial center is serviced by a comprehensive and mature ecosystem. Luxembourg has been responsive to the needs of international investors, and shows a determination to continuously modernize its legal framework. Both attract the international business community. It is this expertise and responsiveness that should continue to secure Luxembourg’s position as a leading financial center. Opportunities in other sectors are blooming in a small, sound, fast reacting and very entrepreneurial country.

Major regulatory change likely to impact the economy

Since 1 January 2015, Luxembourg has switched to the automatic exchange of information between tax authorities under the EU Savings Directive. One of the main consequences for private banking is a loss of clients with “lower” levels of wealth. In the meantime, the typical client profile has changed, as Luxembourg is an increasingly attractive destination for ultra-high net worth individuals.

Another key challenge will be the Organization for Economic Cooperation and Development’s (OECD) Action Plan on Base Erosion and Profit Shifting (BEPS). The BEPS project marks the most significant change to international tax in modern times. The reforms announced by the OECD will have a significant impact on international businesses, whether through greater compliance demands or impacting how they are structured. Luxembourg has embraced transparency, and will act in support of this provided a “level playing field” exists between all major financial centers, reinforcing its attraction to international players. Luxembourg takes the opportunity brought by the higher “substance” requirements required by BEPS to welcome more qualified workers.

Since 1 January 2015, Luxembourg has increased its VAT rates, which may result in extra costs for the country’s economy, possibly affecting activity levels, at least temporarily. Also, changes in the EU VAT rules on e-commerce activities could reduce the arrival of new internet companies How those changes are going to impact the economy is still uncertain. There is a balance between the positive and negative effects, and further factors are likely to emerge in the near future. Some factors have been clearly identified while some others are still at an early stage of evolution, with their outcome not yet known.

Outlook

The real estate market is inevitably driven by the continued success and performance of the economy. A strongly-performing economy will increase the need for office space, and will also attract more foreign employees to the country. More residents and more cross-border employees will also lead to the greater development of retail space.

3- Demographic changes drive further demand

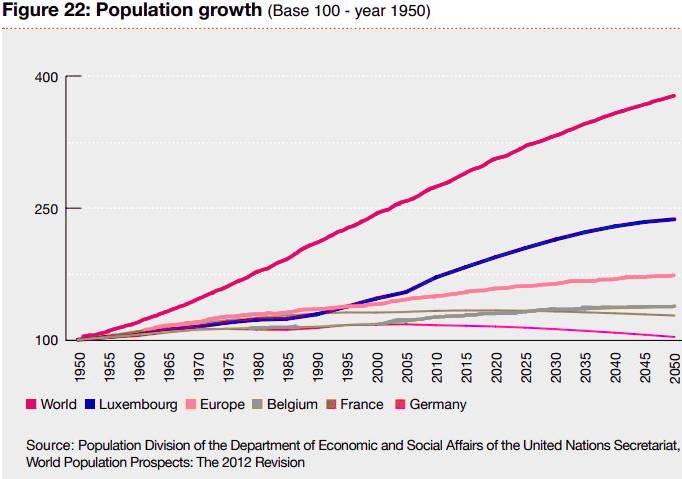

– The Luxembourg population has grown by more than 40% in 25 years

– The Luxembourg population will reach 700,000 people between 2045 and 2050

Population to grow and more foreigners to come

The Luxembourg population grew at the same pace as its European neighbors until 1990.

Since then, the population has grown by more than 40% in 25 years, outperforming even global population growth (38%) over the same period.

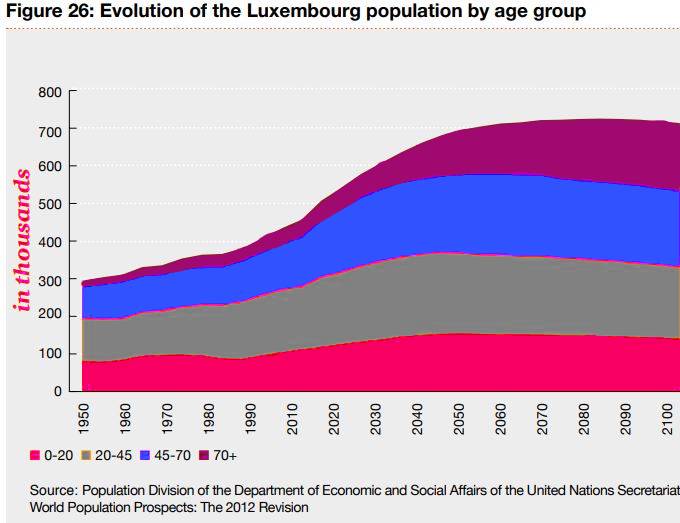

This trend is set to continue for the coming decades since the need for a growing workforce will exceed the current population in Luxembourg. As a consequence, natural population growth will be supplemented by the arrival of newcomers to the country. Furthermore, the number of cross-border workers who will relocate to Luxembourg is expected to increase, due to changing tax rules in adjoining countries, and to the desire to avoid spending hours in congested traffic. In this context, the UN forecasts that the population of Luxembourg will reach 700,000 between 2045 and 2050. With such an increase, the country will have to develop its land-use strategy, both in terms of future dwelling location, and for infrastructure development.

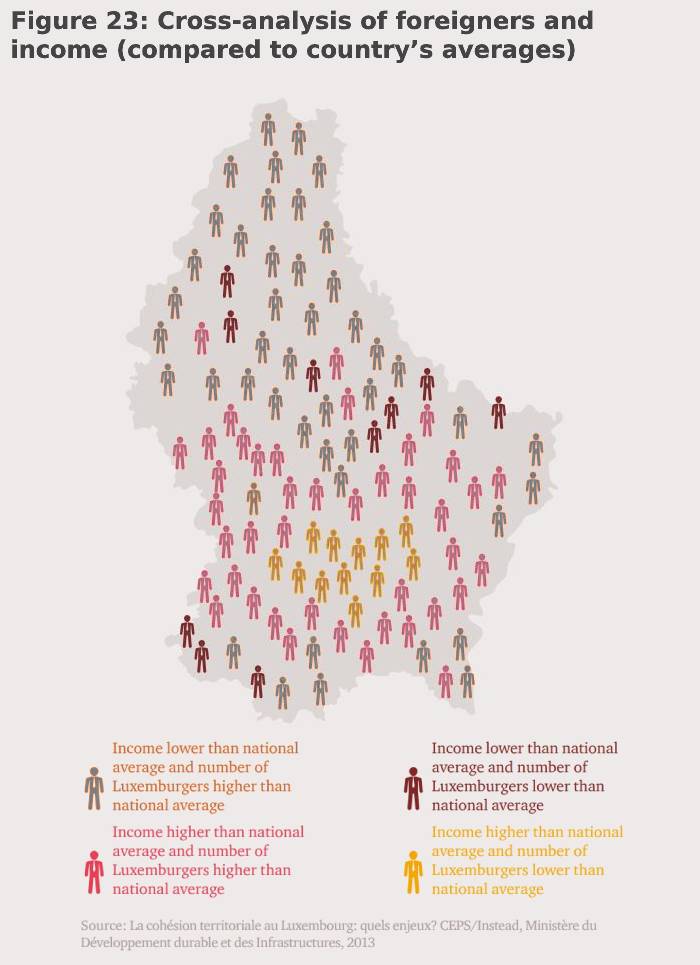

Wealthy foreigners push Luxembourg nationals out of the city

Luxembourg City and its vicinity gather the highest number of wealthy foreigners, while the northern part of the country has more Luxembourg nationals. Foreigners can afford high rents in the City whereas most nationals own their main residence, and are mostly located outside the City.

The “ripple” effect generated by Luxembourg’s high property market has led nationals, in search of a more cost-effective deal, to leave the country to move abroad. Case in point: the number of nationals living abroad and commuting to Luxembourg to work increased by 50%, to 4,500 in 2013 from 3,000 in 2008.

In addition, wealthy retired Europeans, in search of high living standards, have recently increasingly based themselves in Luxembourg City, contributing to the price increase.

All together, these elements might be seen as a threat to social cohesion. Indeed, there could be increasingly significant social differences between Luxembourg City and its surroundings. The Luxembourg middle class is now more inclined to sell houses and land to wealthier people, and to move away from the central areas. The Luxembourg government is aware of this new kind of social issue and some measures, especially in terms of social housing, aim at avoiding a high discrepancy in the country’s social landscape.

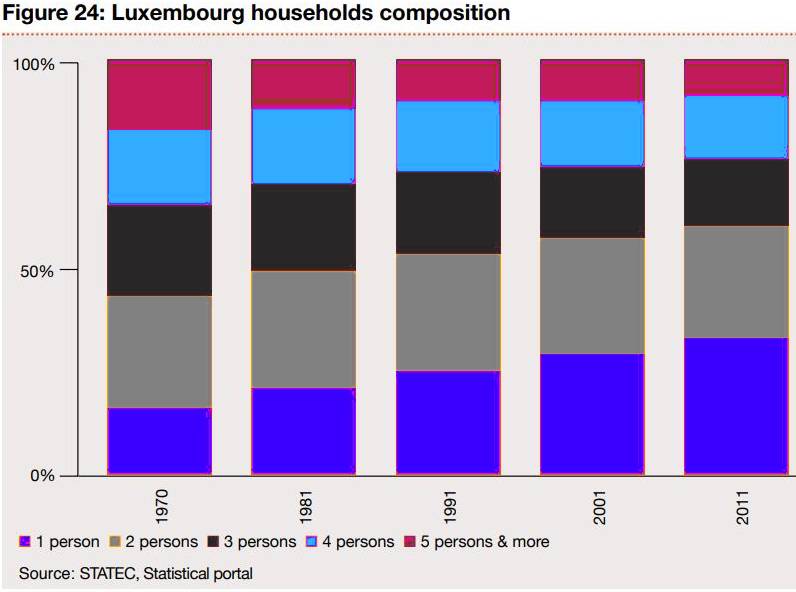

Change in household composition leads to change in residential landscape

Over the last 40 years, household composition has dramatically changed both globally and in Luxembourg. The number of people per household has decreased from 3.1 to 2.4 in this period. This change has had a significant impact on the stock of residential real estate, especially in terms of surface area. This trend is set to go on, since the share of foreign residents, with smaller households, coming to Luxembourg is poised for growth. These newcomers are often single or childless couples, and tend to rent their accommodation when they arrive in Luxembourg. In 2011, 45% of Belgian, French and German residents were single, whereas this figure was only 38% in 2001.

Luxembourg has also one of the highest surface areas per accommodation unit in Europe, with an average of 144 sqm per housing, compared to the European average of 105 sqm. But Luxembourg has also one of the highest rates of under-occupancy (60%), i.e. housing with living space and number of rooms higher than the household’s needs. This percentage is above 80% for people older than 65 years. This under-occupancy is a high concern for the Luxembourg authorities, since the current residential stock is not optimized and cannot meet the strong demand, leading to a global price increase in residential market.

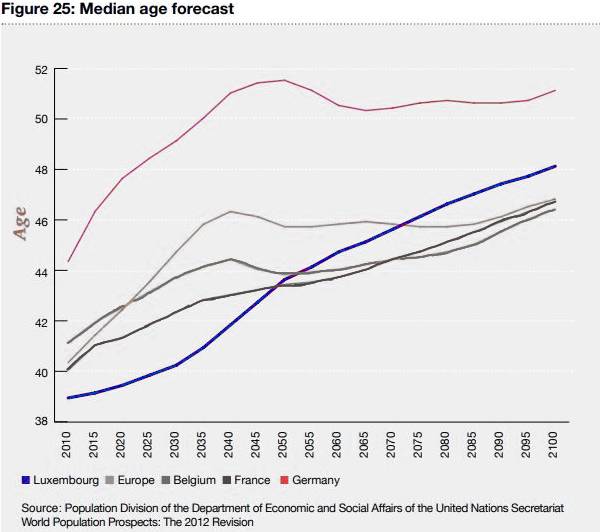

A population set to age faster than neighbors

Even though the median age of the Luxembourg population (39 year-old) is currently one of the lowest in Europe, the size of the older generations will grow faster than in the past. The country’s median age will even overtake that of France and Belgium as from 2050. This surge in the number of elderly people will therefore be accompanied by a further need for retirement and nursing homes. This trend has already been apparent: there were more than 5,000 people in such homes in 2011, double the figure for 2001. Home care services have developed at a rapid pace over recent years; but with life expectancy increasing, nursing homes will have a greater role to play in the long term. In addition, Luxembourg elderly population should be able to afford such services.

Outlook

The landscape for residential real estate has changed over recent decades, and will keep on evolving. Developers are taking into account the needs of newcomers as:

– More apartments than houses are being built.

– The surface area of dwellings will decrease slightly, with new delivery being more functional.

There will be competition between wealthy people for large houses in Luxembourg City and its surroundings. The quality of accommodation is also a factor: some buyers purchase old houses in order to renovate them throughout, or even to demolish and build a completely new home.

4- Technology and sustainability will change the real estate landscape

– Luxembourg tops EU list of internet use with over 94% of households having internet access

– 13% of the office stock has already obtained green certifications

How online retail impacts real estate

Technology impacts real estate, especially in the retail sector. Luxembourg is one of the most internet-connected countries, with about 94% of households having internet access against less than 75% in EU on average. From 2008 to 2012, online purchases in Luxembourg increased by 58%: Luxembourg had the highest rate of online purchase of books and magazines in EU.

The high online purchase rate in Luxembourg is partly explained by its large foreign population, ordering online to get products only readily available abroad. Other internet services have been developed in the country over the last years. For instance, many stores are now providing time-efficient solutions such as “Pick & Go” and home delivery services. This means that shopping centers are being driven to reinvent themselves, to become entertainment places. By offering such services, Luxembourg will still attract tourists and citizens for shopping. However, in such a context, logistics business needs will become increasingly important. This trend follows the Government intention to develop logistics services. The central location of the country within Europe, together with strong exports and the good development of railway infrastructure, are competitive advantages for the country in attracting logistics companies.

Green buildings and eco-friendly accommodation are becoming more common

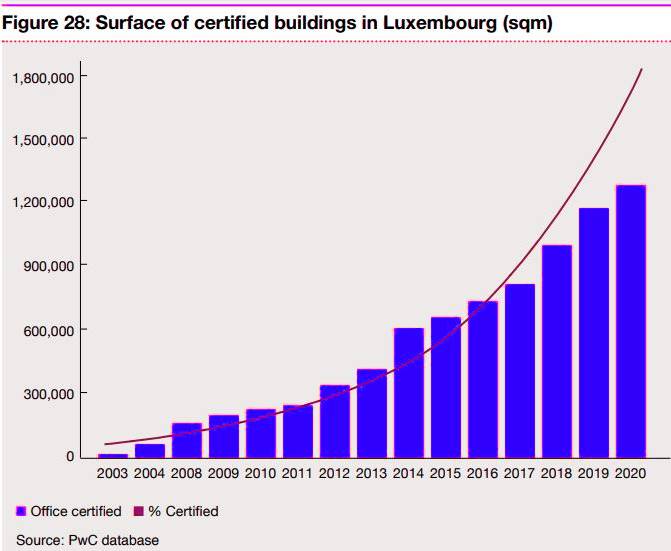

Luxembourg is at the forefront of sustainability choices for properties. Currently, more than 13% of the office stock has already obtained some form of green certification. This proportion will continue to grow, given that most current new office buildings and the future pipeline are planned to be eco-efficient, and many existing office owners are also seeking green certifications.

Luxembourg office stock is younger than the European average, and has more often been built in compliance with the latest sustainability standards. This trend is also the same for residential properties, since the market for so-called passive houses (i.e. energy-efficient house, reducing its ecological footprint, especially for space heating and cooling) has grown over the last few years, with Luxembourg planning regulations also encouraging such kind of construction.

In addition, the new EU regulation on energy performance of buildings, coming into force in 2020, will accelerate the trend for green buildings.

Outlook

Technology and sustainability have already impacted real estate and this trend is set to continue. Retailers will need to adapt to new consumption habits, and those who will most appropriately mix physical and online sales will be successful. Logistic centers will also grow, with the expected further increase in online shopping. Luxembourg has undeniable advantages in this area, thanks to its location, and the Government will further encourage the development of this type of activity.

Green is the future. Tenants are more and more concerned with ecology matters, meaning that green buildings will be more readily let, and with higher rents, whereas older properties will be subject to a so-called “brown discount”.

5- New sources of financing for real estate

– Institutional investors show more and more interest in Luxembourg real estate market

– 22% of Luxembourg households own a net wealth over EUR 1 million

More institutional investors to come

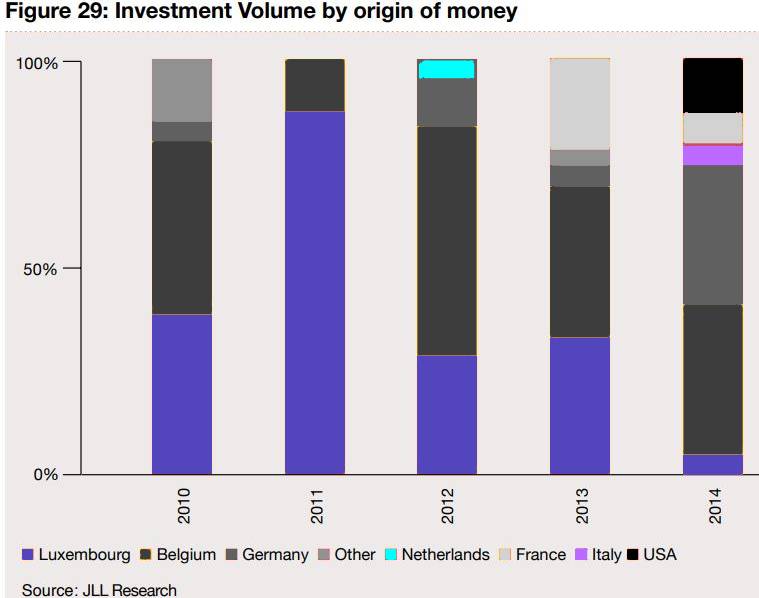

More institutional investors to come Institutional investors are increasingly investigating and entering the Luxembourg real estate market. This trend only really begun a few years ago, and since then the majority of speculative investment has been made by foreign institutional investors. In the past, such investors were quite reluctant to enter the Luxembourg market, given its relatively small size, its lack of transparency, and the limited number of other real estate investors interested in the market.

However, the stability of the country, its positive economic perspective and its proven resilience to the crisis, together with attractive yields offered by office properties, have now become the main drivers for further foreign institutional investment to arrive.

In addition, the quality of the tenants in Luxembourg and the current low vacancy rates are additional positive aspects that institutional investors will consider. Even though there are some suggestions that such investors might still be hesitant to come to Luxembourg, efforts by all parties, including promoters, developers, and government and local authorities, to ease accessibility to, and knowledge of, the market are critical to support the arrival of further new investors.

More foreign private investors to come

There has been an increase in real estate acquisitions in Luxembourg by private bankers and family offices on behalf of their clients. Despite most of these transactions being confidential, with little information publicly available, market sources confirm that family offices are more and more active in this market. The increasing arrival of high-net-worth individuals in Luxembourg will also impact the residential real estate market, since they are ready to pay high prices to buy their homes.

Additionally, the wealth of existing Luxembourg residents is also an important factor to consider. 22% of Luxembourg households have net wealth of over EUR 1 million, which makes it first in Europe, far ahead Switzerland, which is second in the ranking, with 13%.

Outlook

The real estate community will adapt to meet the expectations of large foreign institutional investors and make the country attractive for them. The favorable perceptions of some investors will have a snowball effect, and other investors will then increasingly have Luxembourg on their radar. As demand will be higher than supply, new projects should be emerging as opportunities for investment.

For more information please contact us:

Home Office:

+352-27765002

(Between 07:00 A.M and 9:00 A.M)

Tel:

++352-691-500009

Email:

wm@wissammobayyed.eu