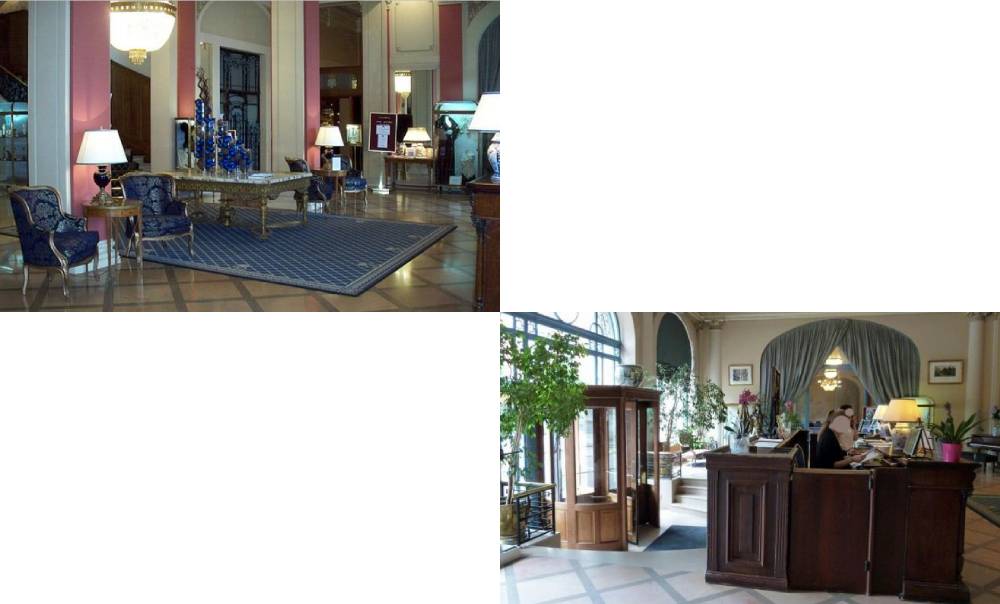

The Aletti Palace is situated in the prime residential area of Vichy, across the opera, and very close to all the historic and important sites like the Opera, town hall, the river allier, sporting stadiums, commercial areas and the thermal Spa.

The Aletti Palace is considered the “hotel de ville” and is the most grand hotel built in Vichy. Built by Joseph Aletti, France’s most famous Hotelier, is the only hotel

carrying his name. Mr. Aletti built and owned amongst others the Clardige in Paris, the hotels Negresco, Majestic, des Anglais and Hotel Ruhrl in Nice, and the Hotel L’Orient Palace in Menton.

Classification

4 Stars with option to upgrade to 5 stars

Space

10,800 m2

Construction

Built in 1910, a stone building of an “art-déco” style,

completely renovated in 1992 and conserving its

“belle épque” style

No of floors

8 floor, plus a basement and an extra floor for administration.

No of rooms

133 total:

45 standard

30 m2

81 superior

50 m2

7 suites

60 m2

Restaurants

1. Le restaurant La Véranda

80 seats

2. Historic “Le bar ASCOT”

25 seats

3. Pool Restaurant and Bar (Summer)

30 seats

Conference/Salon

Eugénie

220 m2

Napoléon 3rd

110 m2

Winter garden

55m2

Hortense

170 m2

Conference room

1st Floor

50 m2

Conference room

2nd Floor

50 m2

Conference room

3rd Floor

50 m2

Other

Lobby and all Salons with very high ceilings.

General communal spaces.

Exterior pool with accessible terrace for reception area and lobby.

The Spa City of Vichy:

The city of Vichy is located in the Auvergne region in the center of France, south of Paris with a distance of 360 km. It is connected via the main highway and enjoys a direct connection via train (2hrs and 55 minutes). The international airport of Clermont-Ferrand is 90 km away.

Vichy is considered the most important spa city in France and contains three luxury hot water springs and three cold water springs. The city, completely built in the luxurious and charming “Belle Epoque” style boast a beautiful opera, casino, major conference centers and famous horserace tracks.

The city of Vichy has been nominated to seek protection as a UNESCO heritage site due to its history of being the major Spa city in Europe. Emperor Louis Napoleon III made the city famous in the 19th century as his preferred retreat area. Since that time and well into the 1930’s, it has been the prime destination for the upper class in France and the middle east and north Africa.

During the high season from May to September, the city center is filled with international and French tourists that come to visit and rehabilitate themselves in the many medical and therapeutic Spa’s. Countless bars and restaurants are full of life as are shops in the charming and close downtown area. During the

remaining part of the year, the city has specialized in attracting many large corporations that hold conferences and congresses.

Vichy is also very attractive due to its extensive sports possibilities including luxury golf courses, horseracing events on its famous track and river canoeing and racing.

contact us:

Home Office: +352-27765002 (Between 07:00 A.M and 9:00 A.M)

The computer will be located at a data center in Bissen and launched in 2021

Luxembourg has acquired a European ‘supercomputer’ for €30 million which will be launched in 2021, the economy ministry said on Tuesday, part of Europe’s efforts to avoid becoming dependent on technology outside the bloc’s borders.

The Grand Duchy will become home to the computer which can be used in a wide range of areas that need high-performance computing such as predicting weather patterns or designing new medicines.

The computer is part of a project by the European Commission and will be located in Bissen, a town north of Luxembourg city which tech giant Google has earmarked for its own data center, will host one of the high-performance computing machines.

The push to build the powerful computers forms part of the European Union’s efforts to stay on top of digital change and avoid becoming dependent on technology located outside the bloc’s borders.

The EU’s decision to locate a supercomputer in Luxembourg comes after the country was chosen as the headquarters for the legal and financial structure overseeing the creation of a European supercomputer network.

Such computers will also be installed in Bulgaria, the Czech Republic, Finland, Italy, Portugal, Slovenia and Spain.

Europe currently consumes around 29% of all supercomputing resources worldwide but the EU industry only provides around 5% of this – with no EU supercomputer in the top 10 globally.

The Luxembourg supercomputer, co-financed by the EU, will have a power of 10 million billion peta-flops per second, which equates to around 10 million billion calculations per second, the government said.

For more information please contact us:

Home Office: +352-27765002 (Between 07:00 A.M and 9:00 A.M)

Part four: Trends and drivers for real estate’s evolving landscape

Mobility within the country and cross-border countries

International economic perspective for Luxembourg

Demographic changes drive further demand

Technology and sustainability will change the real estate landscape

New sources of financing for real estate

Part One:

Introduction – The future for Luxembourg real estate should follow global trends

The Luxembourg real estate market – On and on goes the growth:

Luxembourg has seen outstanding development over the last decades, outperforming most other European countries. The country’s geographic and demographic characteristics are one of a kind. The combination of these factors has had an enormous impact on the real estate market. And this is set to continue.

The office and residential markets are the country’s main real estate drivers. Judging by the size of the country, their value is massive. Based on our predictions, both the office and residential markets are set to continue to grow until 2020, offering good investment opportunities.

Luxembourg has a lot going for it, especially in terms of security, and political and economic stability. And the future success of its real estate industry will largely depend on these distinctive features. Further development of the infrastructure will be instrumental for the country to remain attractive and at the same time address the changing needs of its residents (both nationals and foreigners). These challenges are at the top of the government’s agenda – many political measures are under way to maintain this privileged quality of life.

Another essential feature for real estate sector growth is the economic stability of the country. The last two years have been a turning point for Luxembourg – the country has taken major economic actions, showing its commitment to moving to enhanced cooperation in taxation and exchange of information. This will undoubtedly attract new arrivals, especially high-net-worth individuals. Taking this into account, GDP projections by both the Luxembourg government, and by supranational bodies such as the International Monetary Fund (IMF), are bullish. Other factors, including technological developments, increasing efforts to support sustainability and new sources of financing, are also expected to help drive the future of the Luxembourg real estate industry

An exciting time for the international real estate sector:

The international real estate sector will be at the center of rapid economic and social changes over the next five years. If well anticipated, real estate players can turn these new challenges into great opportunities.

Interest in real estate is already gaining momentum, as more and more investors allocate a significant share of their assets into real estate investments. Case in point: Standard & Poor proposed to break real estate out of financial assets and turn it into its own sector.

In our report, “Real Estate 2020: Building the future”, we projected that the worth of global institutional grade real estate will expand by more than 55% – from USD 29 trillion in 2012, to USD 45 trillion in 2020. Here are the coming challenges that we identified globally:

Huge expansion in cities, with mixed results

Unprecedented shifts in population driving changes in demand for real estate

Emerging market growth ratchets up competition for assets

‘Sustainability’ transforms design of buildings and developments

Technology disrupts real estate economics

Real estate capital takes financial center stage

Our six predictions for 2020 and beyond

The real estate landscape in Luxembourg will change spectacularly in the coming years. Here, we highlight what we expect to be the main changes to come:

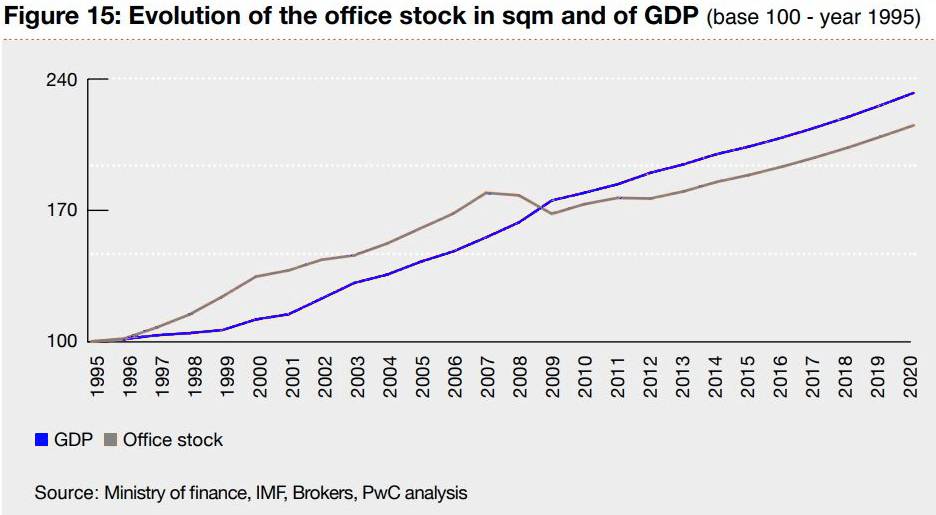

The office and residential markets will grow by nearly 60% and 50% respectively over the period from 2012 to 2020. This growth is driven mainly by economic development and its resulting need for office space and an augmented workforce.

The current volume of office space for rent will not be enough to meet demand. If the economy grows as expected, businesses will be squeezed for office space, and Luxembourg will experience a marked shortage of office properties.

Mobility and infrastructure developments will be crucial to the country. With the projected increase of population and cross-border employee numbers by 2020, infrastructure needs will grow further, and efficient mobility solutions will have to be adopted over a tight timescale in order to keep pace with demands.

The number of foreigners in Luxembourg City and its close neighborhood will keep on increasing, and the residential rental market will expand in this area. A growing number of Luxembourg nationals with lower income will move to surrounding regions within the country, or even move across the borders.

More apartments than houses will be built, in order to best address the needs and budgets of households. The average number of persons by household has significantly decreased over the last decades, and this trend will continue with the arrival of new residents.

New investors, both institutional and private, will come to Luxembourg. Pension funds and other institutional investors will show more interest in operating in the Luxembourg market, and high-net-worth individuals will keep on coming to Luxembourg.

Part Two:

Everything gets bigger in Luxembourg!

This is how we can say how fast the country has developed over the last decades. The growth of both the economy and population has been exponential compared with other EU countries

A fast-growing and competitive economy

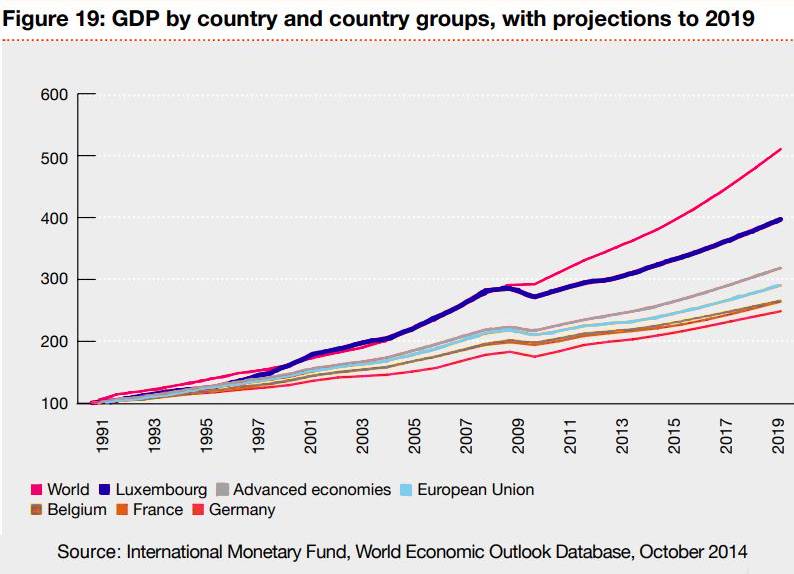

– The workforce has almost doubled in 20 years whereas it increased by less than 20% in Europe

– The Luxembourg GDP has more than tripled from 1991 to 2014 while the Euro zone GDP doubled

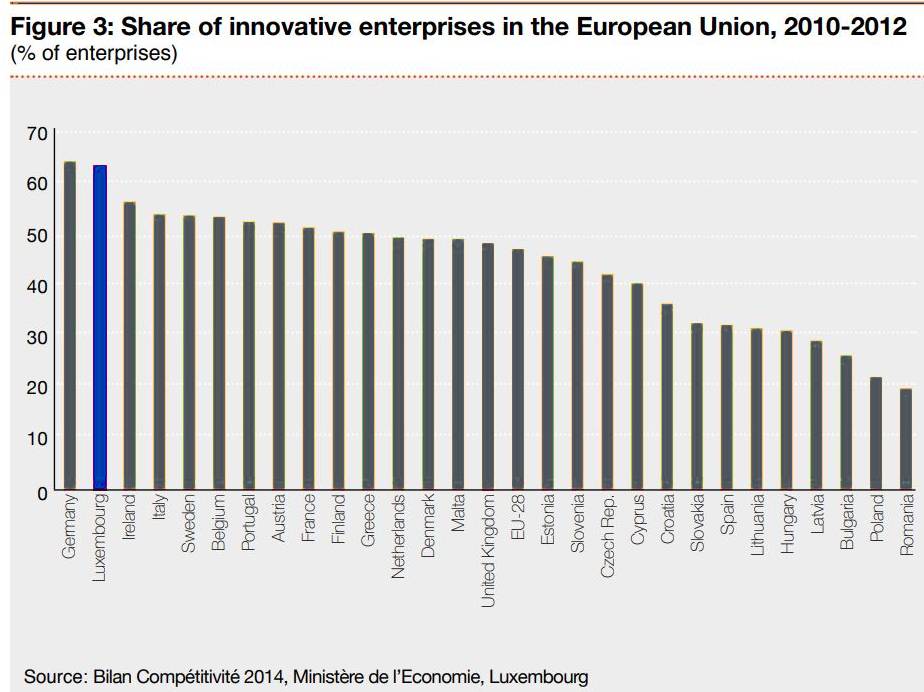

On top of a stable political environment and sound public finances, Luxembourg’s main strength lies in its ability to adapt its economic strategies quickly . Before being a major financial marketplace, Luxembourg was initially an agricultural country. The steel industry then became the bedrock of the country’s economy. As that industry progressively declined, the government saw in financial services new sources of development. As the first EU country to adopt “UCITS” legislation into national law, in 1988, Luxembourg achieved a turning point in its history by becoming a major center for investment funds in Europe and in the world. The Grand Duchy made the most of its expertise in financial services, and quickly became a hub for banks and insurance companies. Nowadays, the financial sector is the strongest component of the Luxembourg economy – nevertheless the country is continuing to diversify its economy by investing in new industries, such as the logistics business and the Information and Communication Technologies (ICT) sector.

As a consequence, the size of the workforce has almost doubled in 20 years, whereas it increased by less than 20% in the European Union (EU) over the same period. In the same vein, Luxembourg’s GDP has more than tripled between 1991 and 2014, while Euro zone GDP merely doubled.

Luxembourg has also been able to attract major multinational groups, and has encouraged them in developing their activities in the country. The ranking of Luxembourg in international competitiveness surveys confirmed its attractiveness. In “The Global Competitiveness Report 2014 – 2015”, the World Economic Forum ranked Luxembourg 19th out of 144, up from 22nd in 2013. In the World Competitiveness Ranking, the country moved from 13th in 2013 to 11th in 2014. In most global surveys, Luxembourg position has moved up compared to their previous findings.

Furthermore, Luxembourg, along with Brussels and Strasbourg, is one of the European Union capitals. Several major EU institutions are headquartered in Luxembourg, such as the European Commission and Parliament, the Court of Justice, the Court of Auditors and the Investment Bank. Many European civil servants work in these institutions, contributing to the development of the country.

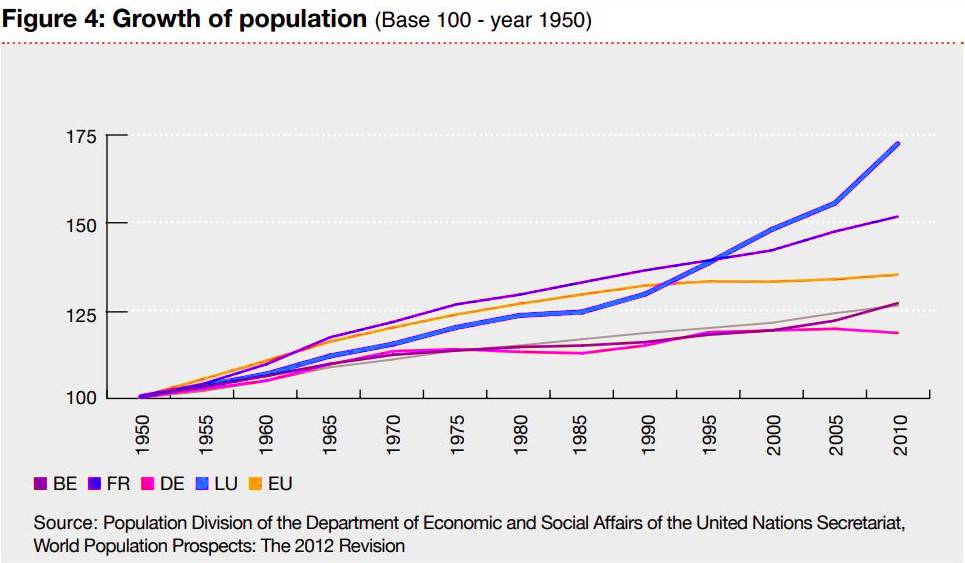

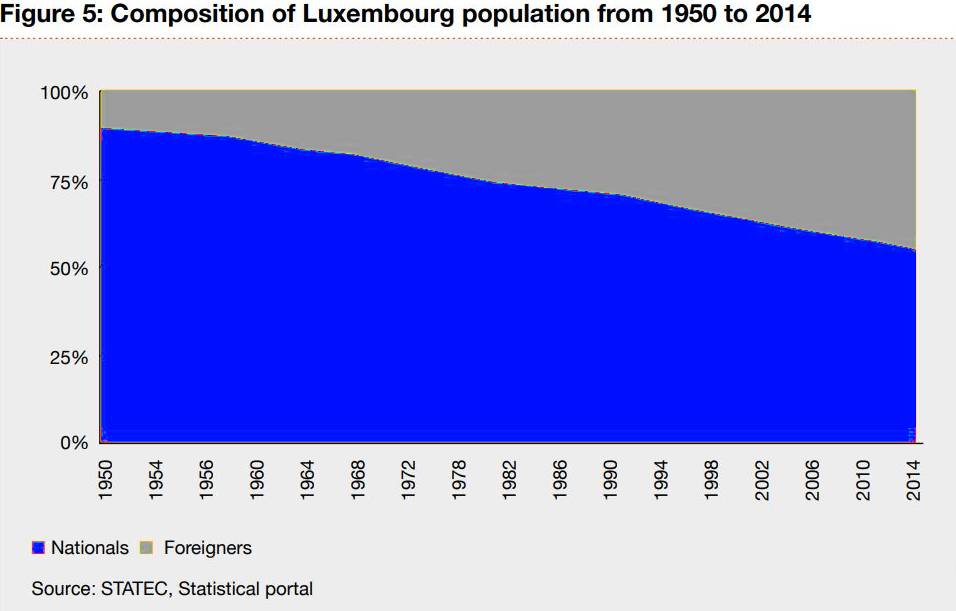

A growing and multicultural population

– The number of non-national residents is one of the highest in Europe, reaching a record high of 45% of the population

– The population grew by more than 70% from 1950 to 2010

The surge in population has been supported by the significant and ongoing arrival of foreigners to meet the needs of the growing economy. As a result, the number of non-national residents is one of the highest in Europe, now amounting to more than 45% of the population. Since 1977, the total number of foreigners living in Luxembourg has tripled5 . Most of these foreigners are coming from the EU, although the share of non-European arrivals is slowly but steadily increasing. This cosmopolitanism turns out to be an asset for the country, since most of the new comers are highly skilled workers. Case in point: The Global Talent Competitiveness Index 2014 ranked Luxembourg third globally in attracting talent.

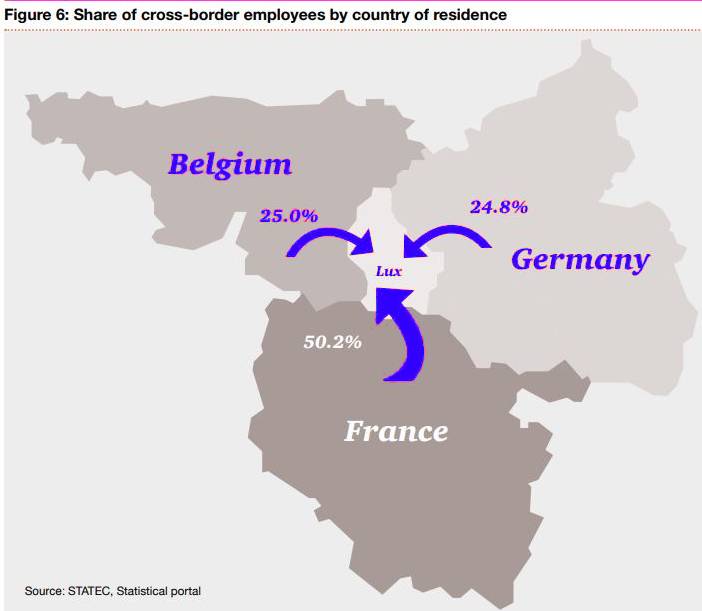

The highest level of cross-border workers in Europe…

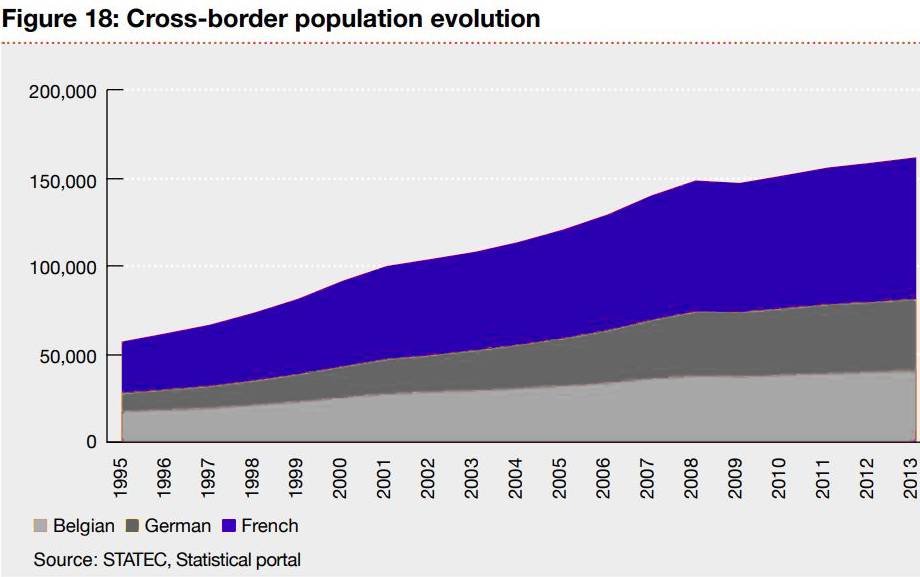

Luxembourg benefits from its central location, with proximity to Germany, Belgium and France. Cross-border workers account for more than 44% of the country’s labor force, contributing enormously to economic growth . The number of cross-border employees has tripled over the last 20 years . Currently, more than 160,000 cross-border workers commute to Luxembourg every day . The largest community of non-Luxembourg nationals commuting to Luxembourg appears to be the French, followed by Belgians and Germans. With the exception of very small countries such as Monaco and Liechtenstein, the level of cross-border workers is the highest in Europe.

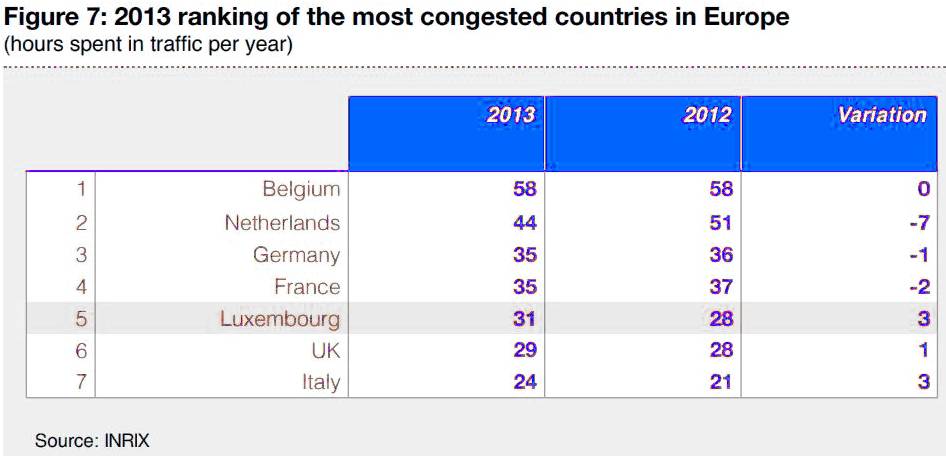

…which results in traffic jam

– The number of cars registered in the country has increased by 35%

– The resident population has increased by 25%

– The cross-border population has grown by 75%

Mobility is at the top of the government agenda. With the growing number of cross-border workers, Luxembourg has become one of most congested countries in the world, ranking 9th on the INRIX scorecard in 2014, from 14th in 2010. Even despite substantial efforts having been made to encourage cross-border workers to use public transport, most still commute by car. The road network has remained virtually unchanged since 2000, whereas the number of cars registered in the country has increased by 35%, the resident population by 25%, and the cross-border worker population by 75%.

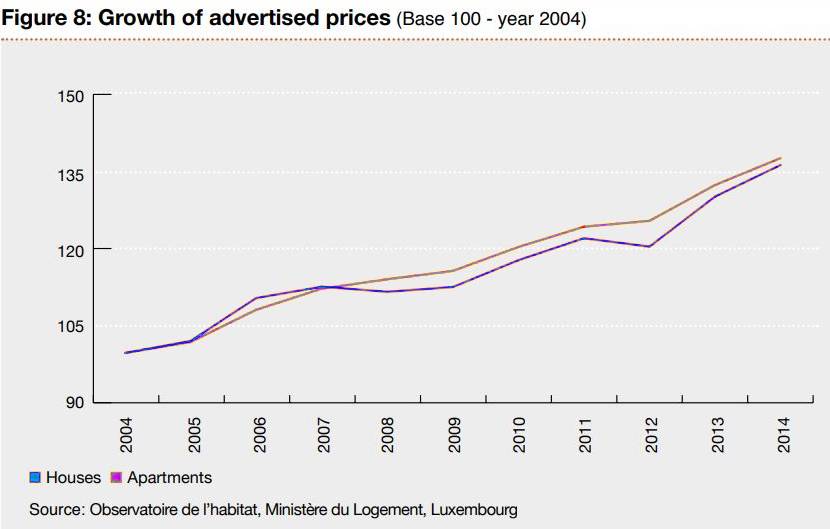

An expensive place to live

With such a surge in population, the demand for property has inevitably increased. The delivery of new dwellings for the last ten years has not met the needs of the growing population completely. As a consequence, the prices of both houses and apartments have risen by more than 35% since 2004.

In 2014, the average price for a house rose by 7% and that of an apartment by 2.9% compared to the previous year.

Living close to work is increasingly expensive. Luxembourg households spend over a third of their monthly expenses on housing, the highest rate in Europe.

Owner-occupiers are driving the residential market

– 85% of national residents own their house

– 50% of foreigners own their accommodation

Most Luxembourg residents own their primary residence. With nearly 71% of home ownership, Luxembourg is in line with the European average and Belgium (72%). However, there are significant discrepancies with neighboring countries, since home ownership stands at 64% in France and 53% in Germany. Such differences are even more significant within the country with about 85% of national residents owning their housing, against approximately 50% for foreigners.

A limited speculative office supply

The office market is highly correlated to the fast-growing economy of the country. As the need for new office spaces keeps on increasing, vacancy levels in Luxembourg’s central areas are low, and most office deliveries are pre-let, or pre-sold, before completion. Only a few investors are currently developing speculative office projects. However the risk of not finding tenants is quite limited, given that the demand for office space remains high.

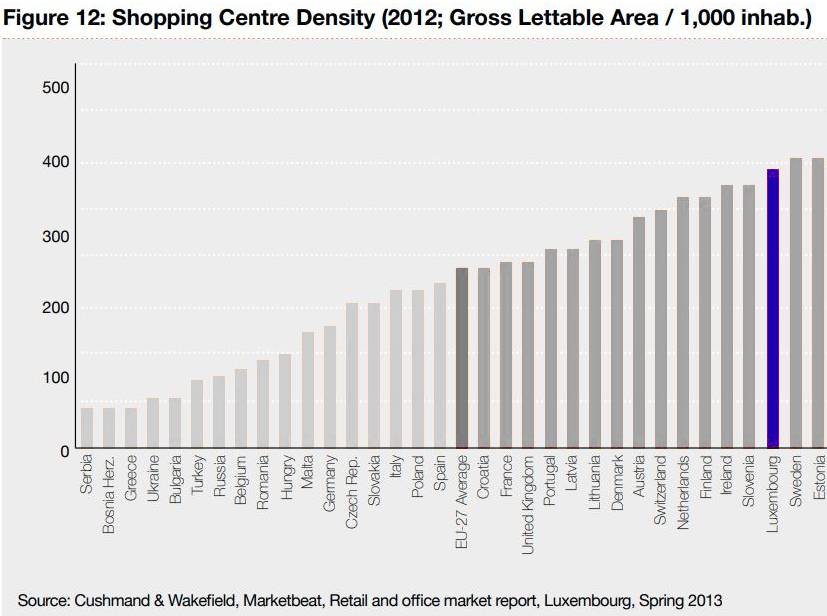

High shopping center density, serving the Greater Region

– The shopping center density per inhabitant in Luxembourg is one the highest in Europe

– The total surface taken up by major retail centers is predicted to surge by approximately 80,000 sqm by 2017, an increase of 16%

Shopping center density per inhabitant in Luxembourg is one of the highest in Europe. Nevertheless, the retail market still has some room for growth, since shops can increasingly tap into a large and growing base of customers coming from the Greater Region, as workers on week days and at weekends with their families.

With an estimated 500,000 sqm, shopping center area is already higher per head in Luxembourg than in almost all other EU countries. The total surface area of major retail centers is predicted to surge by approximately a further 80,000 sqm by 2017, an increase of 16%.

Part Three:

What does 2020 and 2021 have in store?

Although hit by the global financial crisis, both the office and residential markets are now again offering many interesting investment opportunities.

Our methodology

Based on information publicly available, we have determined the total value of the office and residential markets from 2004 to 2012, and developed our own projections for 2020. To do so, we factored in economic forecasts as published by the Luxembourg administration and other supranational bodies, and combined these with projections for population growth, other economic and demographic factors, and real estate brokers’ data.

1- Office Market

– By 2020, the office market will reach EUR 32 billion from EUR 23 billion in 2014, a 40% increase

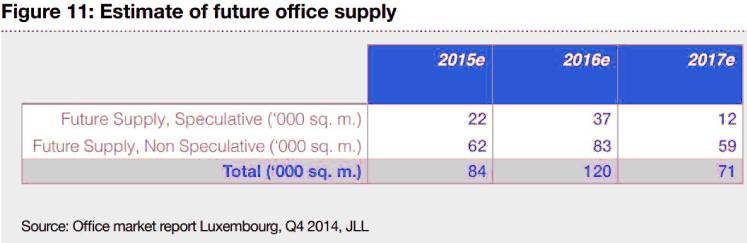

– By 2020, Luxembourg will experience a marked shortage of office properties

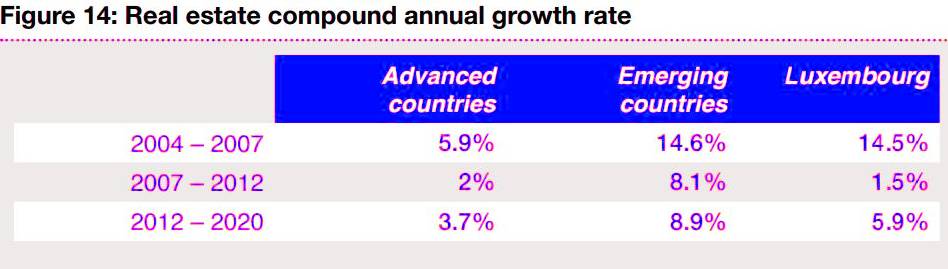

The total value of the office market in Luxembourg has been estimated to be around EUR 23 billion in 2014. Based on our projections, we expect this market to grow by a compound annual rate of 5.9% until 2020, reaching a total value of some EUR 32 billion.

Historically, with an annual increase of more than 14%, the value of the office market soared from 2004 to 2007. Hit by the global financial crisis, market growth slowed to 1.5% per year from 2007 to 2012.

How does Luxembourg real estate compare?

After a short-lived drop from 2007 to 2012, the Luxembourg property market’s growth has surged again, amidst a recovering economy. Despite being described as an advanced country, Luxembourg economic outlook is closer to the projected performance of many emerging countries.

Luxembourg combines the features of an advanced economy and the dynamism of an emerging country

A crunch in office space as demand rises

With Luxembourg’s economic recovery, office leasing activity is now at its highest since 2012. As relatively little new office space is now being developed, we predict a coming supply crunch. The current volume of office space for rent will not be enough to meet demand, given that the vacancy rate stands at approximately 4% and may dip to 3% or below. As rising demand meets a lack of new development, office rents will automatically increase. In such a context, it is likely that the landlords will renegotiate more aggressively the rents of most prized properties.

On the one hand, this analysis should recognize some elements that could mitigate this predicted crunch in office space:

changes in use of in-office space (open working areas are increasingly becoming the norm, and hence the number of sqm per employee decreases), and

The increase of teleworking, which may be poised for growth with the further development of IT.

On the other hand, we have not taken account of any obsolescence within the current office stock, despite it being clear that the current tenants of old and non-eco-friendly properties are likely to move out, and that these properties will need to be refurbished in order to be re-let, or will have to be demolished.

These projected levels of demand and supply will lead to an increase in rent, and to further development of office properties in the suburbs, where there is currently lower rent and easier access. This is likely to attract institutional investors, who will see an opportunity for both regular cash inflow from rents and for capital appreciation.

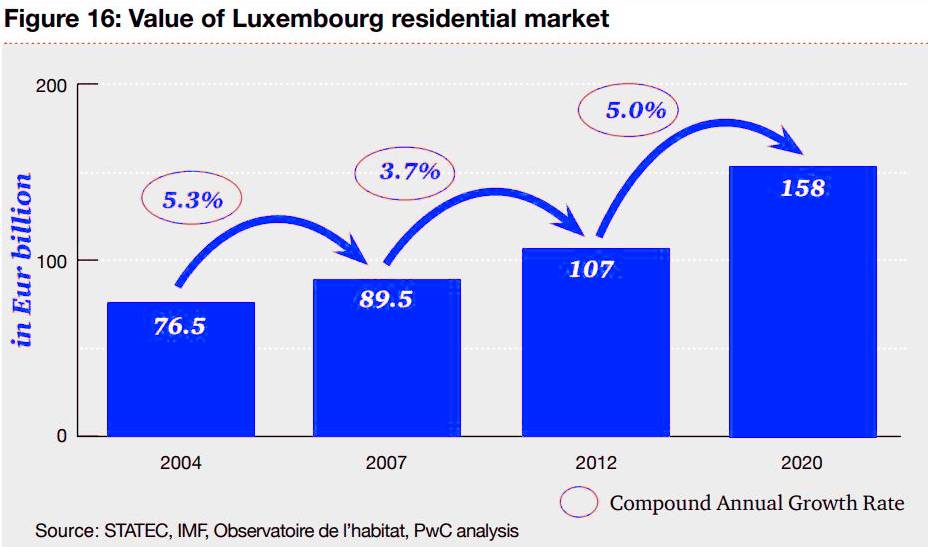

2- Residential Market

– By 2020, the residential market will reach EUR 158 billion, from EUR 122 billion in 2014, a 30% increase

– VAT hike, from 3% to 17%, combined with mismatch of dwelling supply and high demand will keep prices high

Within the Luxembourg real estate market, residential is by far the strongest. Its total value was over EUR 122 billion in 2014, and it will continue to grow at a compound annual rate of 5%, to nearly EUR 158 billion by 2020.

Since 2004, the residential market has grown steadily. The Luxembourg residential market was only moderately hit by the global economic crisis of 2008. Factors affecting the situation include:

The population of Luxembourg has been increasing steadily since 2004.

Demand has remained high, especially for apartments, which are more expensive per sqm than houses.

Dwelling supply has generally not met the increase in demand.

Building standards in Luxembourg are among the highest in Europe and the related costs of construction increased as well.

Inflation has remained relatively high, with an average rate of 2.6% from 2004 to 2013.

Prices on the rise

With dwelling supply not fully addressing the increase in demand, which will now take years to match, prices have boomed. The 14 point increase in VAT, from 3% to 17%, will exacerbate this tendency. (On 1 January 2015, the VAT rate for construction and repair costs was raised to 17% for non-owner-occupied properties.) To counterbalance the higher investment cost, residential property investors will seek to raise rents. However, the increase in the price of property for sale and residential rents may not immediately move in line with the VAT rise.

The rental market is mainly concentrated in Luxembourg City and its neighboring areas. It primarily focuses on apartment letting. Residential property is mostly owned by private investors, as it is a long-held Luxembourgish habit to invest in bricks and mortar.

Part Four :

Trends and drivers for the evolving real estate landscape

We have identified the main trends and drivers which will change the real estate landscape considerably in the coming years. This overview could be a vital aid in planning for the medium-term future.

1- Mobility within the country and cross-border countries

Priced out: More and more people are moving to the suburbs

– Wider spaces are available

– Prices are more affordable

– Teleworking is spreading

Unaffordable rent and lack of offer push people away from the capital

Over the last 20 years, the total population of Luxembourg has increased by 40%, and the number of foreign residents has doubled. This significant surge in population has resulted in domestic migration. From 2005 to 2011, Luxembourg City experienced a negative net migration. More than 7,500 city inhabitants, i.e. almost 9% of the city population in 2005, turned their back on the capital. Soaring prices and lack of suitable properties have caused a surge in the number of people fleeing Luxembourg City to flock to the suburbs. In addition, Luxembourg City is moving slowly from being a residential ownership market to a rental market, encouraging people who want owner occupation of a property to move away from the city.

Working from home is becoming easier and easier, backed by IT solutions. And this adds to this domestic migration trend. But ultimately, despite all the above factors, the population of Luxembourg City increased by 30% over the period from 2005 to 2014. This growth has been mainly driven by the arrival of foreigners in the city.

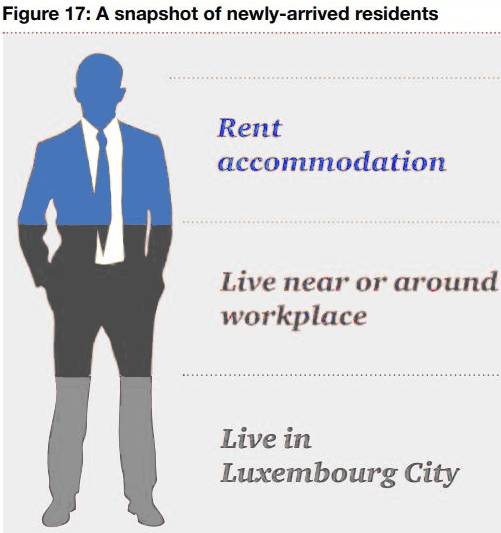

Luxembourg City is mainly attracting foreigners

With most newcomers living near or around their workplace, this being most often located in Luxembourg City, demand for rental properties in the capital has soared, and rental prices have increased correspondingly

Global urbanization – Luxembourg makes no exception

Globally, millions of people are migrating from country to city. Through to 2020, this migration will continue. The cities will swell – and some entirely new ones will spring up. Luxembourg is no exception. Over the last decade, the urbanization of the country has been more marked than ever. From 2001 to 2014, 51% of the country’s population growth has been concentrated in the ten biggest communes, whereas it was only 19% over the period from 1970 to 2001.

This trend was even more marked over the last four years, as 55% of the total growth was in these top 10 communes from 2011 to 2014.

In Luxembourg, 19% of the population lives in the capital. But nearly 45% of the total population lives in the ten biggest communes in the country.

This trend will strengthen in the coming years, since the future delivery of apartments, being mainly located in the larger communes, will be higher than delivery of houses. In addition the government plans to rationalize the country’s landscape, preserving some areas from any construction, while intensifying urbanization in some other areas.

The need for cross-border employees will increase further

To meet the need for a growing workforce, Luxembourg companies increasingly have to tap into cross-border resources. As accommodation prices are high, the newcomers often live abroad, which raises the number of cross-border workers.

Based on our projections and the expected economic growth, the number of cross-border employees will grow by 25% over the next six years, up from approximately 160,000 in 2014 to more than 200,000 in 2020.

Outlook

Infrastructure development and mobility solutions are proving vital for urban success and a high quality of life in Luxembourg. Residential areas located close to work premises, and those connected to infrastructure and the public transportation network, will likely see their prices increase faster than residential properties in regions less well-connected. The rental market in Luxembourg City is expected to grow strongly, since it will remain the first choice for newcomers to Luxembourg

2- International economic perspective for Luxembourg

– Luxembourg’s GDP will grow by 23% from 2014 to 2019

– Luxembourg navigated the storm with a 5-year average growth of 2.5%, compared with 0.6% for the euro area and 1.6% for ‘AAA’ peers

A positive outlook towards 2020

The world is facing significant challenges: economically, politically and socially. Luxembourg can rely on its financial stability and triple A credit rating to face challenges looming on the horizon. The country has navigated the storm and performed well throughout the global financial crisis, with a five-year average growth of 2.5%, compared with 0.6% for the euro area.

With a growth forecast aligned with other advanced economies, and still ahead of the other main EU countries, Luxembourg’s economic future looks positive.

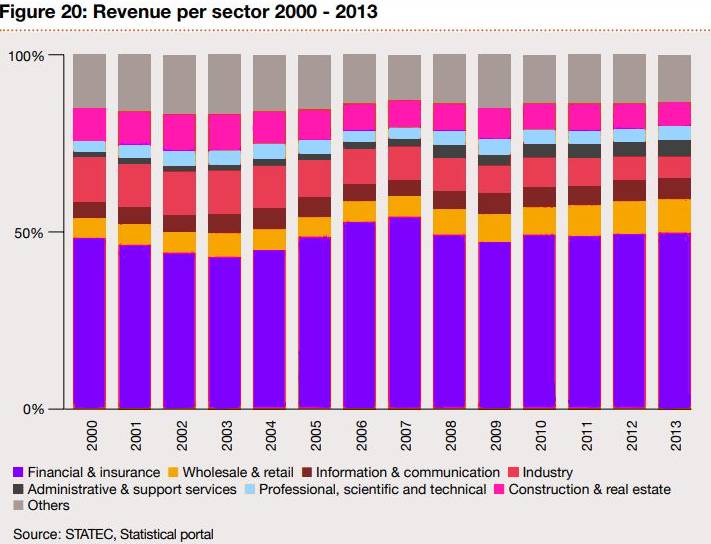

The financial sector will continue to be the main growth engine

The financial services sector, including banking and insurance services represent approximately 50% of the total revenue for the country. In contrast, the share of the revenue attributable to heavy industry has halved since 2000.

The share for wholesale and retail business, and administrative and support services, increased from 7% in 2000 to 16% in 2013. In spite of a sustained level of activity, construction and real estate services saw its share decreasing to 7% in 2013.

Even if some sectors have gone through important changes, the financial sector remains the main driver of the country’s economy. This also means that the national economy is more exposed to global financial shocks. But it also still constitutes an opportunity. Over the last three decades, Luxembourg has developed as an international financial center that is globally recognized for its high level of expertise. This financial center is serviced by a comprehensive and mature ecosystem. Luxembourg has been responsive to the needs of international investors, and shows a determination to continuously modernize its legal framework. Both attract the international business community. It is this expertise and responsiveness that should continue to secure Luxembourg’s position as a leading financial center. Opportunities in other sectors are blooming in a small, sound, fast reacting and very entrepreneurial country.

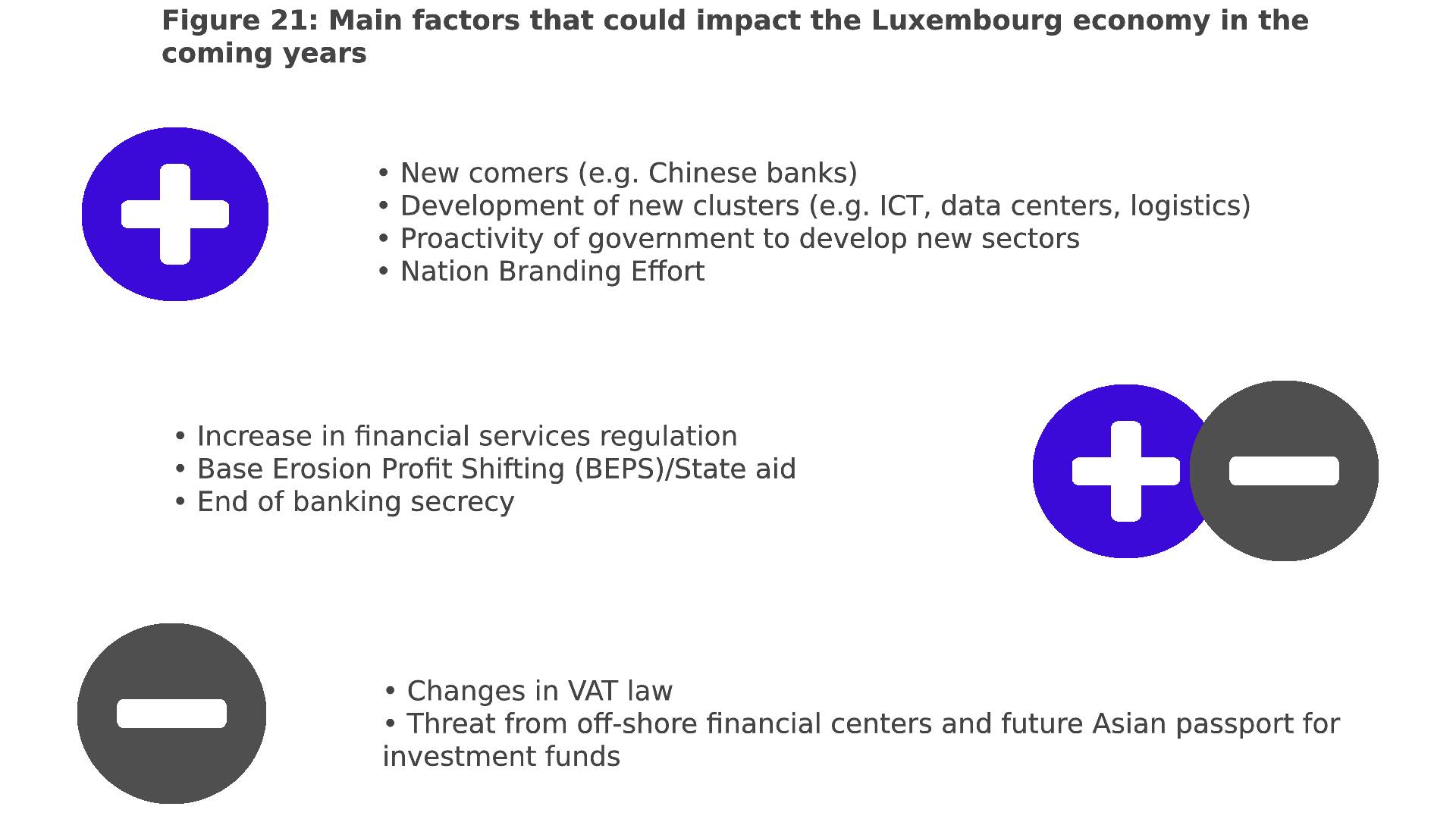

Major regulatory change likely to impact the economy

Since 1 January 2015, Luxembourg has switched to the automatic exchange of information between tax authorities under the EU Savings Directive. One of the main consequences for private banking is a loss of clients with “lower” levels of wealth. In the meantime, the typical client profile has changed, as Luxembourg is an increasingly attractive destination for ultra-high net worth individuals.

Another key challenge will be the Organization for Economic Cooperation and Development’s (OECD) Action Plan on Base Erosion and Profit Shifting (BEPS). The BEPS project marks the most significant change to international tax in modern times. The reforms announced by the OECD will have a significant impact on international businesses, whether through greater compliance demands or impacting how they are structured. Luxembourg has embraced transparency, and will act in support of this provided a “level playing field” exists between all major financial centers, reinforcing its attraction to international players. Luxembourg takes the opportunity brought by the higher “substance” requirements required by BEPS to welcome more qualified workers.

Since 1 January 2015, Luxembourg has increased its VAT rates, which may result in extra costs for the country’s economy, possibly affecting activity levels, at least temporarily. Also, changes in the EU VAT rules on e-commerce activities could reduce the arrival of new internet companies How those changes are going to impact the economy is still uncertain. There is a balance between the positive and negative effects, and further factors are likely to emerge in the near future. Some factors have been clearly identified while some others are still at an early stage of evolution, with their outcome not yet known.

Outlook

The real estate market is inevitably driven by the continued success and performance of the economy. A strongly-performing economy will increase the need for office space, and will also attract more foreign employees to the country. More residents and more cross-border employees will also lead to the greater development of retail space.

3- Demographic changes drive further demand

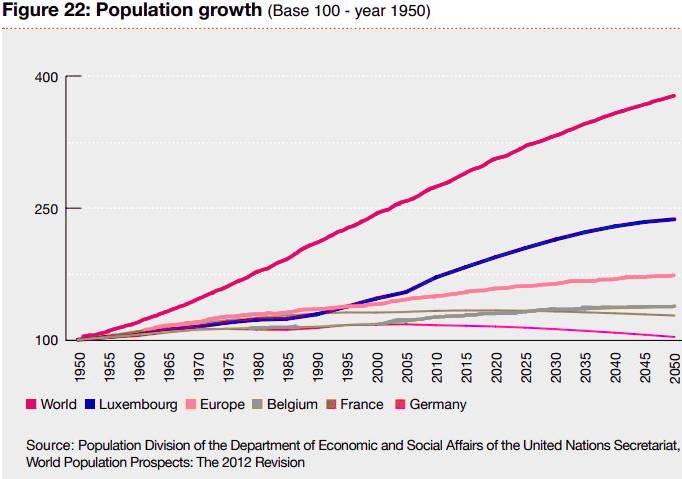

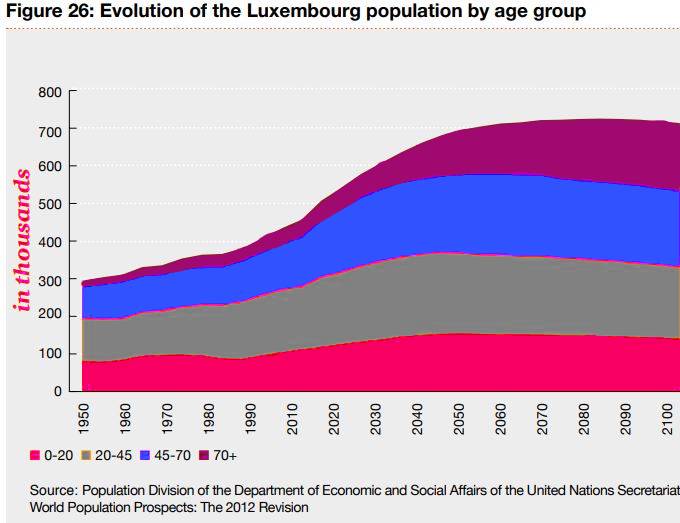

– The Luxembourg population has grown by more than 40% in 25 years

–The Luxembourg population will reach 700,000 people between 2045 and 2050

Population to grow and more foreigners to come

The Luxembourg population grew at the same pace as its European neighbors until 1990.

Since then, the population has grown by more than 40% in 25 years, outperforming even global population growth (38%) over the same period.

This trend is set to continue for the coming decades since the need for a growing workforce will exceed the current population in Luxembourg. As a consequence, natural population growth will be supplemented by the arrival of newcomers to the country. Furthermore, the number of cross-border workers who will relocate to Luxembourg is expected to increase, due to changing tax rules in adjoining countries, and to the desire to avoid spending hours in congested traffic. In this context, the UN forecasts that the population of Luxembourg will reach 700,000 between 2045 and 2050. With such an increase, the country will have to develop its land-use strategy, both in terms of future dwelling location, and for infrastructure development.

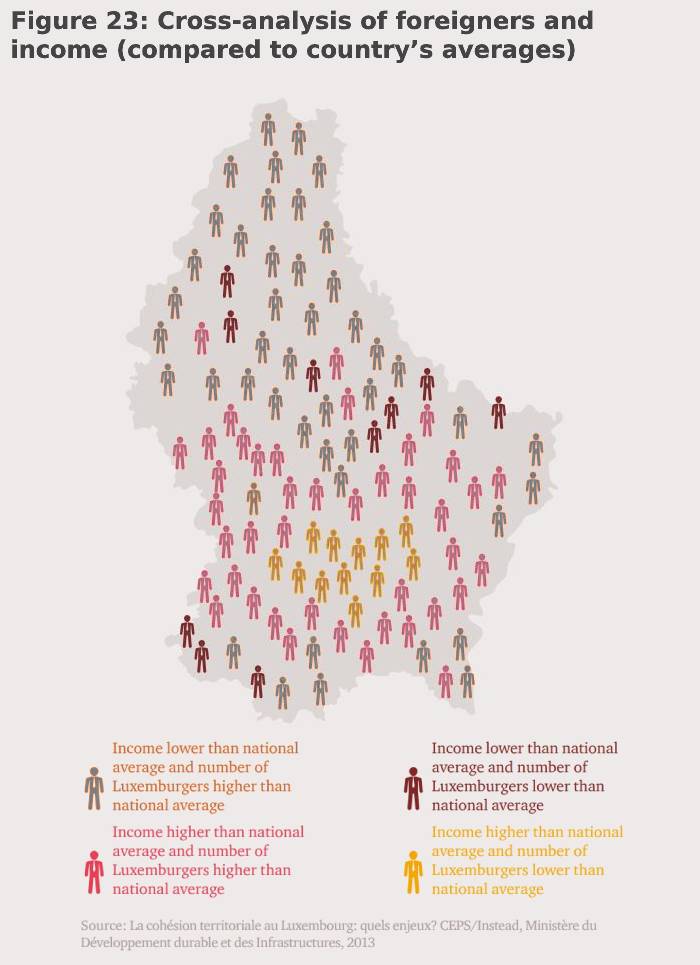

Wealthy foreigners push Luxembourg nationals out of the city

Luxembourg City and its vicinity gather the highest number of wealthy foreigners, while the northern part of the country has more Luxembourg nationals. Foreigners can afford high rents in the City whereas most nationals own their main residence, and are mostly located outside the City.

The “ripple” effect generated by Luxembourg’s high property market has led nationals, in search of a more cost-effective deal, to leave the country to move abroad. Case in point: the number of nationals living abroad and commuting to Luxembourg to work increased by 50%, to 4,500 in 2013 from 3,000 in 2008.

In addition, wealthy retired Europeans, in search of high living standards, have recently increasingly based themselves in Luxembourg City, contributing to the price increase.

All together, these elements might be seen as a threat to social cohesion. Indeed, there could be increasingly significant social differences between Luxembourg City and its surroundings. The Luxembourg middle class is now more inclined to sell houses and land to wealthier people, and to move away from the central areas. The Luxembourg government is aware of this new kind of social issue and some measures, especially in terms of social housing, aim at avoiding a high discrepancy in the country’s social landscape.

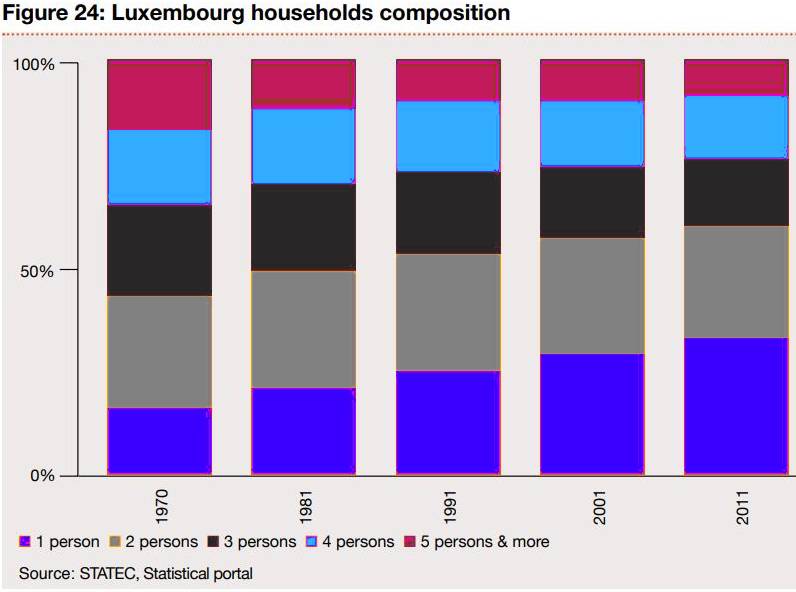

Change in household composition leads to change in residential landscape

Over the last 40 years, household composition has dramatically changed both globally and in Luxembourg. The number of people per household has decreased from 3.1 to 2.4 in this period. This change has had a significant impact on the stock of residential real estate, especially in terms of surface area. This trend is set to go on, since the share of foreign residents, with smaller households, coming to Luxembourg is poised for growth. These newcomers are often single or childless couples, and tend to rent their accommodation when they arrive in Luxembourg. In 2011, 45% of Belgian, French and German residents were single, whereas this figure was only 38% in 2001.

Luxembourg has also one of the highest surface areas per accommodation unit in Europe, with an average of 144 sqm per housing, compared to the European average of 105 sqm. But Luxembourg has also one of the highest rates of under-occupancy (60%), i.e. housing with living space and number of rooms higher than the household’s needs. This percentage is above 80% for people older than 65 years. This under-occupancy is a high concern for the Luxembourg authorities, since the current residential stock is not optimized and cannot meet the strong demand, leading to a global price increase in residential market.

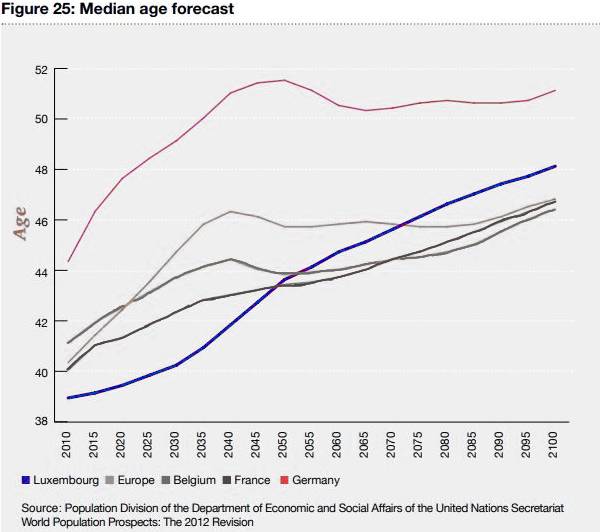

A population set to age faster than neighbors

Even though the median age of the Luxembourg population (39 year-old) is currently one of the lowest in Europe, the size of the older generations will grow faster than in the past. The country’s median age will even overtake that of France and Belgium as from 2050. This surge in the number of elderly people will therefore be accompanied by a further need for retirement and nursing homes. This trend has already been apparent: there were more than 5,000 people in such homes in 2011, double the figure for 2001. Home care services have developed at a rapid pace over recent years; but with life expectancy increasing, nursing homes will have a greater role to play in the long term. In addition, Luxembourg elderly population should be able to afford such services.

Outlook

The landscape for residential real estate has changed over recent decades, and will keep on evolving. Developers are taking into account the needs of newcomers as:

– More apartments than houses are being built.

– The surface area of dwellings will decrease slightly, with new delivery being more functional.

There will be competition between wealthy people for large houses in Luxembourg City and its surroundings. The quality of accommodation is also a factor: some buyers purchase old houses in order to renovate them throughout, or even to demolish and build a completely new home.

4- Technology and sustainability will change the real estate landscape

– Luxembourg tops EU list of internet use with over 94% of households having internet access

–13% of the office stock has already obtained green certifications

How online retail impacts real estate

Technology impacts real estate, especially in the retail sector. Luxembourg is one of the most internet-connected countries, with about 94% of households having internet access against less than 75% in EU on average. From 2008 to 2012, online purchases in Luxembourg increased by 58%: Luxembourg had the highest rate of online purchase of books and magazines in EU.

The high online purchase rate in Luxembourg is partly explained by its large foreign population, ordering online to get products only readily available abroad. Other internet services have been developed in the country over the last years. For instance, many stores are now providing time-efficient solutions such as “Pick & Go” and home delivery services. This means that shopping centers are being driven to reinvent themselves, to become entertainment places. By offering such services, Luxembourg will still attract tourists and citizens for shopping. However, in such a context, logistics business needs will become increasingly important. This trend follows the Government intention to develop logistics services. The central location of the country within Europe, together with strong exports and the good development of railway infrastructure, are competitive advantages for the country in attracting logistics companies.

Green buildings and eco-friendly accommodation are becoming more common

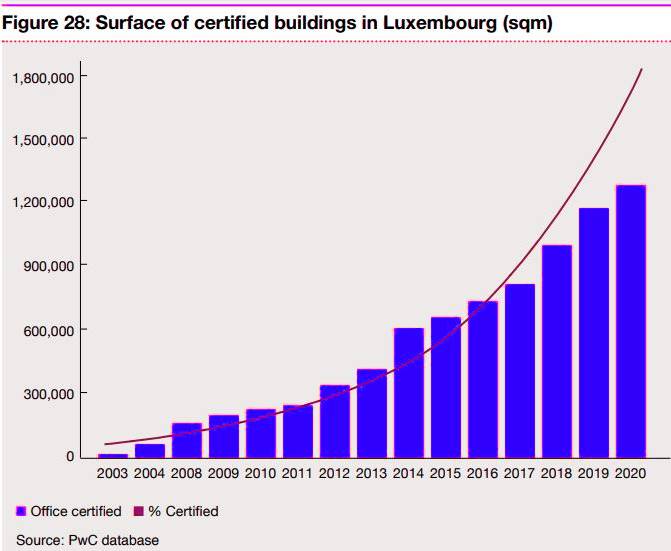

Luxembourg is at the forefront of sustainability choices for properties. Currently, more than 13% of the office stock has already obtained some form of green certification. This proportion will continue to grow, given that most current new office buildings and the future pipeline are planned to be eco-efficient, and many existing office owners are also seeking green certifications.

Luxembourg office stock is younger than the European average, and has more often been built in compliance with the latest sustainability standards. This trend is also the same for residential properties, since the market for so-called passive houses (i.e. energy-efficient house, reducing its ecological footprint, especially for space heating and cooling) has grown over the last few years, with Luxembourg planning regulations also encouraging such kind of construction.

In addition, the new EU regulation on energy performance of buildings, coming into force in 2020, will accelerate the trend for green buildings.

Outlook

Technology and sustainability have already impacted real estate and this trend is set to continue. Retailers will need to adapt to new consumption habits, and those who will most appropriately mix physical and online sales will be successful. Logistic centers will also grow, with the expected further increase in online shopping. Luxembourg has undeniable advantages in this area, thanks to its location, and the Government will further encourage the development of this type of activity.

Green is the future. Tenants are more and more concerned with ecology matters, meaning that green buildings will be more readily let, and with higher rents, whereas older properties will be subject to a so-called “brown discount”.

5- New sources of financing for real estate

– Institutional investors show more and more interest in Luxembourg real estate market

–22% of Luxembourg households own a net wealth over EUR 1 million

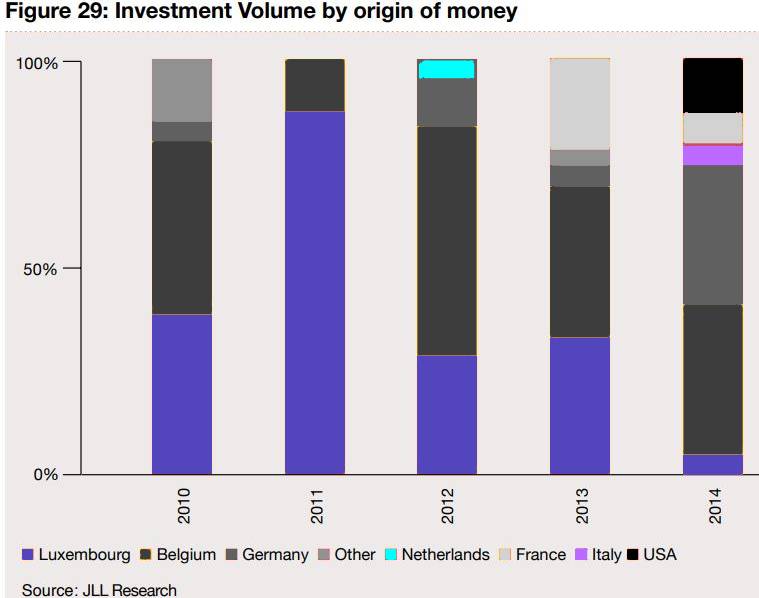

More institutional investors to come

More institutional investors to come Institutional investors are increasingly investigating and entering the Luxembourg real estate market. This trend only really begun a few years ago, and since then the majority of speculative investment has been made by foreign institutional investors. In the past, such investors were quite reluctant to enter the Luxembourg market, given its relatively small size, its lack of transparency, and the limited number of other real estate investors interested in the market.

However, the stability of the country, its positive economic perspective and its proven resilience to the crisis, together with attractive yields offered by office properties, have now become the main drivers for further foreign institutional investment to arrive.

In addition, the quality of the tenants in Luxembourg and the current low vacancy rates are additional positive aspects that institutional investors will consider. Even though there are some suggestions that such investors might still be hesitant to come to Luxembourg, efforts by all parties, including promoters, developers, and government and local authorities, to ease accessibility to, and knowledge of, the market are critical to support the arrival of further new investors.

More foreign private investors to come

There has been an increase in real estate acquisitions in Luxembourg by private bankers and family offices on behalf of their clients. Despite most of these transactions being confidential, with little information publicly available, market sources confirm that family offices are more and more active in this market. The increasing arrival of high-net-worth individuals in Luxembourg will also impact the residential real estate market, since they are ready to pay high prices to buy their homes.

Additionally, the wealth of existing Luxembourg residents is also an important factor to consider. 22% of Luxembourg households have net wealth of over EUR 1 million, which makes it first in Europe, far ahead Switzerland, which is second in the ranking, with 13%.

Outlook

The real estate community will adapt to meet the expectations of large foreign institutional investors and make the country attractive for them. The favorable perceptions of some investors will have a snowball effect, and other investors will then increasingly have Luxembourg on their radar. As demand will be higher than supply, new projects should be emerging as opportunities for investment.

For more information please contact us:

Home Office: +352-27765002 (Between 07:00 A.M and 9:00 A.M)

An individual taxpayer qualifies as a Luxembourg resident when they have their tax domicile or usual abode in Luxembourg.

Nationality is irrelevant when determining tax residence.

The tax domicile is the permanent place of residence that the individual actually uses and intends to maintain.

Individual taxpayers with no tax domicile in Luxembourg will qualify as residents is their usual abode is located in Luxembourg.

To qualify for “usual abode” status, a person needs to be continually present in Luxembourg for six months (short absences are disregarded).

This six-month presence can overlap two calendar years.

The residence applies as from the first day of presence.

Luxembourg residents are taxable on their worldwide income.

Non-resident taxpayer

An individual taxpayer qualifies as a non-resident of Luxembourg if neither their tax domicile nor their usual abode is located in Luxembourg.

Luxembourg non-residents are taxable only on their Luxembourg source income.

Non-resident taxpayers are in principle not entitled to the same range of deductions available to Luxembourg resident taxpayers. Non-residents who are taxable in Luxembourg on more than

90% of their worldwide income or, alternatively, whose income taxable outside Luxembourg does not exceed EUR 13,000, can opt to be treated as if they were Luxembourg residents. For Belgian residents, the option regime can be applied if 50% of their household’s professional income is

taxable in Luxembourg. The option regime allows non-resident individuals to deduct expenses via their Luxembourg income tax return that they would not otherwise be entitled to deduct. The option

regime is not mandatory and must be requested by a taxpayer by filing an income tax return. The tax benefit of the option regime has to be considered on a case-by-case basis.

Tax year

In Luxembourg, the tax year corresponds to the calendar year – 1 January to 31 December.

What if my family remains in my home country?

If your family remains in your home country, the tax authority should refer to the relevant double tax treaty, if any, to determine your tax residence.

Income subject to taxation

The categories of income, after deduction of related expenses, are aggregated to determine the “net” total income. The categories of income are:

Employment income;

Self-employment income;

Dividend and interest income;

Capital gains;

Pension and annuity income;

Rental and royalty income;

Business income;

Agriculture and forestry income;

Miscellaneous income.

The “net income” is then reduced by various deductions in order to determine the taxable income.

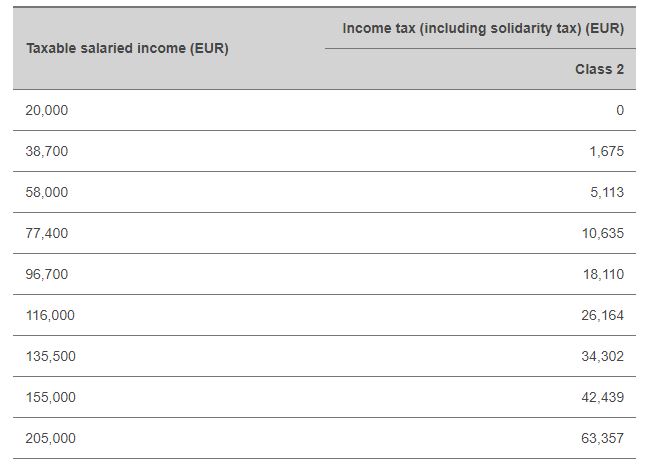

Tax rates

Income tax rates are progressive. They vary from 0% up to 42%. A 7% surcharge for the employment Fund applies on the income tax due. This surcharge amounts to 9% for taxpayers in tax classes 1 and 1a whose taxable income exceeds EUR 150,000 (EUR 300,000 for taxpayers in

tax class 2).

Tax classes

The calculation of Luxembourg income tax also depends on the applicable tax class, which is established according to the individual’s personal situation. There are three tax classes: 1, 1a and 2.

Yearly net taxable income

Tax liability depending on tax class

EUR 30,000

EUR 60,000

EUR 120,000

EUR 240,000

Tax class 1

EUR 2,791

EUR 13,916

EUR 39,168

EUR 92,665

Tax class 1a

EUR 1,277

EUR 13,159

EUR 38,411

EUR 91,908

Tax class 2

EUR 678

EUR 5,584

EUR 27,833

EUR 78,337

Residents

Non-residents

Tax class 2

Married taxpayers

Married taxpayers, subject to conditions and

upon specific request

Widowed persons for the three years following the year in which they became widowed

Same as residents

Divorced or separated individuals for the three years following the year of divorce or separation

Same as residents

Civil partners who live together for a full tax year who elect to file jointly and have a recognized partnership in place for the

full year

Same as residents, subject to conditions

Tax class 1a

Widowed persons not included in tax class 2

Same as resident

Individuals aged at least 65 on 1 January

Same as residents if specific conditions are met

Single parents where the child forms part of their household

Same as residents

Tax class 1

Taxpayers not included in tax classes 1a or 2

Same as residents

Married taxpayers if they have opted for separate taxation

Among others, married taxpayers who have not

opted for joint taxation

Tax treatment for married non-resident taxpayers

Married non-resident taxpayers will be regarded as being in tax class 1 by default, and can no longer be in tax class 1a or 2, even if they have dependent children.

As an exception to this, married non-resident taxpayers may request joint taxation under tax class 2 (i.e. as for married resident taxpayers), provided that at least one of the following conditions is met:

90% of the worldwide income of one spouse is taxable in Luxembourg. When assessing whether this is the case, the first 50 days that are not taxable in Luxembourg according to a double tax treaty are treated as income taxable in Luxembourg;

The income of one taxpayer taxable outside Luxembourg does not exceed EUR 13,000;

For Belgian residents, the rules are less restrictive: only 50% of the household’s professional income needs to be taxable in Luxembourg.

This option can be requested via either payroll or the individual tax return. Non-resident married taxpayers will have to report their non-Luxembourg sourced income (for example, the spouse’s

professional income). Such non-Luxembourg sourced income will be exempt for Luxembourg tax purposes but will be taken into account when determining the applicable tax rate for the Luxembourg

sourced income (“exemption with progression”).

In practice, married non-resident taxpayers where one spouse works outside of Luxembourg and/or where the individual has extensive income outside of their Luxembourg employment income, will be adversely affected by this provision, as it will increase their effective tax rate.

Option to file jointly or individually

Resident jointly taxable taxpayers and married non-residents fulfilling the conditions stated above can either file a joint tax return or opt for separate individual taxation. The application of the selected

regime can be anticipated through payroll.

Under this regime, married couples opting for separate taxation will be allocated tax class 1. They will be able to apply for one of the following regimes:

Full individualization (“individualization pure”), where each item of income is allocated individually to each partner based on the applicable matrimonial regime, and where deductions (e.g. for insurance premiums, interest payments, dependent children) and the potential increase in limits for married couples with dependent children are split equally between the spouses.

Individualization with reallocation of income (“individualisation avec réallocation des revenues”), where the total adjusted taxable household income (determined based on the aggregate net income and applicable tax deductions) will by default be allocated equally between spouses,

irrespective of the level of their individual income. The spouses can also request a different allocation of the total adjusted taxable income.

Payroll withholding tax

Depending on the tax regime chosen, income tax will be withheld through payroll as follows:

Full individualization: each taxpayer is taxed under tax class 1.

Individualization with reallocation of income: taxation at a fixed rate (corresponding to the estimated overall tax rate based on each spouse’s reallocated worldwide income).

Married non-residents opting for taxation through tax class 2 rates: taxation at a fixed rate (corresponding to the estimated overall tax rate based on the household’s worldwide income).

Married non-residents who do not opt for a specific regime: taxation under tax class 1.

Tax return

The application of a fixed rate through payroll (e.g. in the case of individualization with reallocation of income or the application of tax class 2 for non-residents) will trigger an automatic obligation to file a tax return in Luxembourg. Any discrepancy between the estimated

payroll tax rate and the tax rate calculated via the final income tax return may result in additional tax liability or a tax refund, depending on the individual situation.

Should I file jointly with my spouse?

Yes, in principle. Married taxpayers normally file jointly (with specific conditions to be met for non-residents). Civil partners whose partnership agreement is recognized in Luxembourg and who

have been living together for the entire tax year can elect to file jointly (certain conditions apply for non-residents).

However, married taxpayers have the possibility to opt for individual taxation.

What else do I need to know about filing obligations?

In Luxembourg, not all taxpayers have to file an income tax return; but those who do must file it by 31 March of the year following the income tax year (this deadline is usually extended on request).

If the taxpayer is not subject to a filing obligation, a simplified request for a refund of excess withholding tax may be filed under certain conditions. The purpose of such a request is to obtain a refund of excess payroll tax (if any). This request must be filed by 31 December of the

year following the income tax year.

The elements taken into consideration to determine whether a taxpayer has to file an income tax return or request for a yearly calculation are:

His/her residency status;

His/her tax class;

His/her level of income;

The nature of income;

The number of days worked in Luxembourg;

Whether a fixed tax rate has been applied through payroll.

2- Employment income:

Taxable employment income generally includes all benefits in cash or in kind earned from an employment activity. The taxable value of benefits in kind is assessed at the fair market value (i.e. the cost that the employee would have paid if paying for the benefit directly).

However, the Luxembourg Income Tax Law provides for a lump-sum valuation method and exemptions for certain benefits in kind:

Luncheon vouchers

The taxable benefit per voucher is equal to EUR 2.80 for a voucher value of up to EUR 10.80. The taxable basis is reduced to the extent that the employee contributes to the related cost.

Company car

The taxable fringe benefit generated by the private use of a company car is equal to the private mileage multiplied by the kilometer cost of the car. The employee must maintain a logbook recording private mileage. Alternatively, a lump-sum valuation method is available, according to which the monthly taxable fringe benefit corresponds to a rate ranging from 0.5% to 1.8% (depending on the vehicle’s CO2 emissions and fuel type) applied to the price of the new vehicle, reduced by any

discount granted (options and VAT included).

Free accommodation

The taxable fringe benefit amounts to the monthly rent and other rental charges paid by the employer. A reduction of 25% is applied to the rent, subject to certain conditions (the reduction does not apply to other rental charges), and a reduction of 17.5% is applied if the accommodation provided is furnished.

Interest subsidy by the employer

A loan granted by the employer at an interest rate lower than 1.5% generates a taxable fringe benefit. The taxable benefit corresponds to the difference between the 1.5% rate and the discounted interest rate.

Interest subsidies paid by the employer apply where the employer provides financial support in connection with loan interest that the employee has with a third party. The interest subsidy by the

employer generates a taxable fringe benefit in the hands of the employee.

The above benefits are tax-exempt up to EUR 3,000 for mortgage loans related to the acquisition of a main residence and up to EUR 500 for other personal loans. These tax-exempt amounts are doubled for taxpayers filing jointly and single taxpayers with dependent children.

Occupational pension schemes

The employer’s contributions to a qualifying occupational pension scheme are subject to a flat tax rate of 20% to be borne by the employer. Benefits received are tax-exempt in Luxembourg.

Specific income tax exemptions

Gifts by the employer based on the employee’s seniority with the company. The exemption varies between EUR 1,120 and EUR 4,500.

Overtime pay and extra pay for working nights, Sundays or public holidays.

Severance pay (conditions apply).

Employment-related expenses

Professional expenses related to employment income are tax-deductible. A yearly lump-sum deduction of EUR 540 is allocated to all employees. This deduction can be replaced by real expenses incurred (evidence should be provided). In addition, commuting expenses are deductible

based on the distance between the employee’s home and workplace. The maximum deduction for commuting expenses is EUR 2,574 per year.

3- Directors’ fees:

Gross directors’ fees, whether they are paid to a resident or non-resident director, are subject to withholding tax at a rate of 20%. The 20% tax is used as a tax credit against final income tax liability assessed on the basis of an income tax return.

The 20% tax withheld is fully discharged for non-resident directors if (i) their gross directors’ fees do not exceed EUR 100,000 and (ii) they have no other Luxembourg-source professional income.

Directors may opt to file an income tax return. In such circumstances, tax is assessed pursuant to progressive income tax rates. Whether a director should file an annual income tax return should be considered on a case-by-case basis.

Please note that VAT applies to the payment of director’s fees.

Individuals deriving more than EUR 100,000 gross Director’s fees per year must carry out a double-entry bookkeeping (on an accrual basis).

4- Dividend and interest income:

Withholding tax of 15% applies to Luxembourg domestic dividends (this withholding tax is not a final discharge of tax).

For final taxation, dividend income is subject to progressive income tax rates. A 50% tax exemption of the gross dividend can be obtained on dividend income paid by a fully taxable company resident in a European Union Member State or a State that has concluded a tax treaty with

Luxembourg.

Interest paid or attributed to a Luxembourg-resident individual by a paying agent located in Luxembourg is subject to 20% withholding tax, which represents a full discharge of the tax.

Resident taxpayers receiving cross-border interest income can also apply for 20% flat rate taxation to the extent that the paying agent is located in another EU Member State or EEA State, provided that they submit a specific request to the tax authority by 31 March 2021 for the 2020 tax year.

Interest payments that do not fall within the scope of the 20% taxation (e.g. income received from a UCITS, interest paid by certain foreign paying agents, etc.) continue to be subject to taxation according to progressive income tax rates via an income tax return. A lump-sum deduction of EUR1,500 (doubled for taxpayers taxable jointly) applies to total dividend and interest income (subject to progressive taxation) received during the tax year.

5- Capital gains

Capital gains on immovable property

Capital gains on the sale of the taxpayer’s main residence are tax-exempt. Capital gains on other real estate property:

are subject to progressive income tax rates if the disposal takes place within two years of acquisition; and

are subject to a reduced tax rate if the disposal takes place more than two years after acquisition. The reduced rate is effectively half of the marginal tax rate. A tax deduction of up to EUR 50,000 (doubled for married taxpayers and civil partners filing jointly) valid every

ten years may be claimed on the capital gain. In addition, a deduction up to EUR 75,000 for inherited property (through the direct line of descendance) may apply.

Under specific conditions, taxation of capital gains from the disposal of property can be deferred if it is used to fund the acquisition of a new property located in Luxembourg that the owner intends to rent out.

Capital gains on movable property

Income tax regime

Short-term capital gains:

Shares are disposed of

within six months of the

acquisition date

Taxation based on Luxembourg progressive income tax rates if total short-term gains for the year amount to at least EUR 500

Long-term capital gains:

Shares are disposed of

more than six months

after the acquisition date

Capital gain is tax-exempt if the taxpayer does not hold a major shareholding (10%)

Capital gain is taxed at a reduced tax rate (max. half marginal tax rate) if the taxpayer holds a major shareholding (10% or more)

A tax deduction of up to EUR 50,000 valid every ten years may be claimed on the capital gain (doubled for married taxpayers and civil partners filing jointly)

6- Real estate income:

Residence occupied by the owner (main residence)

A principal private residence is deemed to have no rental value.

Mortgage interest linked to the property (ceilings applicable) are tax-deductible, as long as the property is the taxpayer’s main residence.

Thresholds applicable to mortgage interest:

EUR 2,000 for the 1st year of occupation and the following 5 years;

EUR 1,500 for the following 5 years;

EUR 1,000 for the following years.

These limits are multiplied by the number of individuals forming part of the taxpayer’s household.

Residence rented out

The net rental income is determined by deducting rental expenses from the gross rental income.

The gross rental income is determined by aggregating any payment made by the tenant to the owner of the property.

Expenses related to rental income:

Debit interest on a mortgage loan;

Insurance (fire, civil liability, etc.);

Property tax;

Repair and maintenance costs, etc.;

Depreciation of construction (amortization rate varies from 2% to 6% depending on the year of construction of the building) and further investments – except land (lump-sum calculation of 20% of the acquisition price if price of land at acquisition is unknown).

Alternatively, if the taxpayer does not have any actual expenses, a lump-sum deduction may be applied.

No deductions apply to a secondary residence located in Luxembourg or abroad.

7- Deductible items:

Special expenses

Mandatory state social security contributions

Mandatory state social security contributions paid to the Luxembourg social security system and contributions paid to a foreign state scheme in accordance with a social security treaty are tax-deductible.

Gifts

Gifts granted to a Luxembourg or EU qualifying institution are tax-deductible if the individual’s qualifying donations exceed EUR 120 p.a. Tax deductibility is limited to EUR 1,000,000 and 20% of total net income.

Employee contributions to an occupational pension scheme

The employee’s contributions to a qualifying occupational pension scheme set up by the employer are tax-deductible up to EUR 1,200 (yearly cap).

Lump sum

A yearly lump-sum deduction of EUR 480 is available for employees (doubled for taxpayers filing jointly, as long as they both earn employment income – see also questions & answers on p.17).

Extraordinary charges

Extraordinary charges are tax-deductible only if they exceed the “normal charge” of the household as determined by Luxembourg tax law. The costs incurred should be unpredictable, unforeseeable and reduce the ability to pay income tax during the year (e.g. medical expenses not reimbursed by the CNS or a mutual fund, legal fees, etc.).

In addition, the costs of child care, household employees and home assistance for disabled individuals are deductible.

Two methods of calculation:

normal charge method (the deduction will depend on your family situation and your level of taxable income); or

lump-sum deduction with a cap of EUR 5,400 on a yearly basis (only applicable for child care, household employees and home assistance for disabled individuals).

Environmentally sustainable transport

A tax deduction is available for environmentally friendly means of transport if purchased after 1 January 2017. It amounts to EUR 5,000 for the purchase of an electric or hydrogen car, and EUR300 for the purchase of an electric or regular bicycle for adults.

Tax credit for employees

Employees are entitled to a tax credit on a yearly basis ranging from EUR 0 to EUR 600 depending on their level of income (applicable to each married spouse and civil partner earning a taxable salaried income).

What type of private expenses can I claim?

The lump sum of EUR 480 for employees can be replaced by actual expenses:

Single death insurance premium related to a mortgage loan

EUR 6,000

Increased by EUR 672 for jointly taxable taxpayers and each dependent child.

Up to the age of 40, it is EUR 1,344. Increased for jointly taxable taxpayers and each dependent child.

Amount per taxpayer subscribing to a private old-age pension scheme.

The deduction can be increased based on the individual’s personal situation (age, number of dependent children, etc.).

Are there any extra deductions for married taxpayers?

Yes. Married taxpayers and civil partners are entitled to a EUR 4,500 tax deduction on a yearly basis if they file jointly 1 and both earn professional income taxable in Luxembourg.

What about deductions for children?

Single parents with dependent children may claim a yearly tax credit ranging from EUR 750 to EUR 1,500 depending on their level of income. Moreover, education and maintenance costs for children who do not qualify as dependent can be deducted by up to EUR 4,020 per child per year.

If the spouses opt for separate taxation (please refer to the section on the tax treatment of married taxpayers), they will each be entitled to a EUR 2,250 tax deduction (married taxpayers only).

8- Social security:

Regular social security contributions

Regular Luxembourg social security contributions consist of an employer and an employee portion.

Both are computed on gross remuneration capped at EUR 10,709.97 per month on 1 January 2020 (EUR 128,519.64 cap per year).1 The following rates are applicable.

Employee’s portion

Employer’s portion

Health

• Periodic remuneration

• Non-periodic remuneration (e.g. bonus)

3.05%

2.80%

3.05%

2.80%

Sickness (employers’ mutual fund)

/

0.46% – 2.70%

Pension

8%

8%

Accident

/

0.675% – 1.125%

Health at work

/

0.11%

Total (periodic remuneration

11.05%

12.295% – 14.985%

Please note that this limit is subject to change depending on developments in the consumer index, which may change in 2020.

Rates applicable for the year 2020.

Depends on the absenteeism rate in the company.

This rate depends on the factor bonus-penalty system and is determined by the “Association assurance accident”.

Or EUR 45/year if the employer is registered with the ASTF.

Mandatory social security contributions borne by the employee are deductible for Luxembourg income tax purposes.

Dependency contribution

In addition to the above-mentioned regular social security contributions, employees are subject to a monthly contribution (“contribution dépendance”) based on the gross remuneration less EUR 6,426

per year for 2020. This contribution amounts to 1.4%. Unlike regular social security contributions, the dependency contribution’s basis is not capped and is not tax-deductible. The dependency contribution is also payable by Luxembourg residents on their patrimonial income if they benefit from Luxembourg health insurance.

Social security benefits

9- Taxation of cross border workers:

As previously indicated, Luxembourg tax residents are taxable in Luxembourg on their worldwide income whereas non tax resident individuals are taxable locally on their Luxembourg source income only. One such source of income would be remuneration paid in connection with a Luxembourg employment contract, on the basis that the individual physically performs the duties of the employment in the territory of Luxembourg.

However, specific rules apply to the taxation of Luxembourg employment remuneration in the hands of non-Luxembourg resident employees if the employee works outside of Luxembourg.

Therefore, if an employee has business trips and trainings outside of Luxembourg, or does home based working, there may be an impact on the taxation of the Luxembourg employment income as well as tax consequences in the country of residence.

In order to establish whether Luxembourg employment remuneration is fully taxable in Luxembourg an individual should refer to the Double Tax Treaty between Luxembourg and their country of residence.

Over the past several years, the Double Tax Treaties (DTT’s) between Luxembourg and border countries (Germany and Belgium) have been amended to include certain tolerance thresholds with regards to non-Luxembourg workdays.

The most recent development is the new DTT signed between Luxembourg and France which entered into force on 1 January 2020.

A summary of the different thresholds and related countries is outlined below.

Country of residence

Threshold

Germany

19 days

Belgium

24 days

France

29 days

As such, if an employee exceeds the above threshold of non-Luxembourg workdays, the income related to those workdays becomes fully taxable in the country of residence – please note that there may even be withholding tax obligations for Luxembourg employers on such

income in the other country.

Correspondingly, the related income should then be exempt from tax in Luxembourg.

In addition to the above tax consequences, there may also be social security obligations arising as a result of non-Luxembourg work days – A1 certificates may need to be obtained, social security obligations may be triggered in other countries etc. Indeed, we see that it is becoming more and more important for employers and their employees to ensure compliance with their tax and social security obligations within the context of cross border working and business travel.

For more information please contact us:

Home Office: +352-27765002 (Between 07:00 A.M and 9:00 A.M)

Individual income tax is levied on the worldwide income of individuals residing in Luxembourg, as well as on Luxembourg-source income of non-residents.

Enlightened by: Wissam Mobayyed

Personal income tax rate

Luxembourg income tax liability is based on the individual’s personal situation (e.g. family status). For this purpose, individuals are granted a tax class. Three tax classes have been defined:

Class 1 for single persons.

Class 2 for married persons as well as civil partners (under certain conditions).

Class 1a for single persons with children as well as single taxpayers aged at least 65 on 1 January of the tax year.

As of 1 January 2018, married non-resident taxpayers who are not separated are granted tax class 1. However, subject to some conditions, they can request to be treated as Luxembourg tax resident to obtain the application of the tax class 2 (generally, the tax class for resident unseparated spouses). The application of tax class 2 leads to a combined assessment.

Non-resident taxpayers may request joint taxation under tax class 2 (i.e. as for married resident taxpayers), provided that at least one of the following conditions is met:

90% of the worldwide income of one spouse is taxable in Luxembourg. When assessing whether this is the case, the first 50 days that are not taxable in Luxembourg according to a double tax treaty (DTT) are treated as income taxable in Luxembourg.

The income of one taxpayer taxable outside Luxembourg does not exceed 13,000 euros (EUR).

For Belgian residents, the rules are less restrictive. Only 50% of the household’s professional income need to be taxable in Luxembourg.

This option can be requested via either payroll or individual tax return. Non-resident married taxpayers will have to report their non-Luxembourg-sourced income (for example, the spouse’s professional income). Such non-Luxembourg-sourced income will be exempted for Luxembourg tax purposes but will be taken into account when determining the applicable tax rate for the Luxembourg-sourced income (‘exemption with progression’).

In practice, married non-resident taxpayers where one spouse works outside of Luxembourg and/or where the individual has extensive income outside of their Luxembourg employment income will be adversely affected by this provision, as it will increase their effective tax rate.

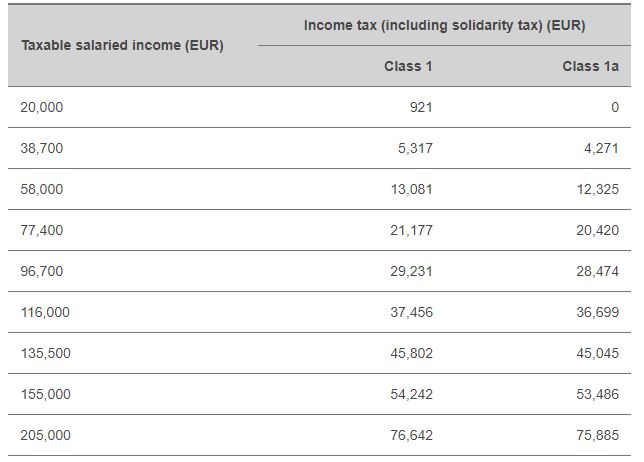

Tax is calculated in accordance with a progressive table, ranging from 8% on taxable income in excess of EUR 11,265 to 42% on income in excess of EUR 200,004 for 2018. A solidarity tax of 7% of taxes (9% for taxpayers earning more than EUR 150,000 in tax class 1 and 1a or more than EUR 300,000 in tax class 2) must also be paid.

Single taxpayer (Class 1/Class 1a) :

Married taxpayer (Class 2) :

For more information please contact us:

Home Office: +352-27765002 (Between 07:00 A.M and 9:00 A.M)

Luxembourg’s participation exemption regime provides for an exemption from income, withholding and net wealth tax for qualifying investments held by qualifying entities. The exemption from income tax is extensive, covering dividends, capital gains and liquidation proceeds.

In addition, no withholding tax applies on dividend distributions if the conditions for the participation exemption are met. Finally, participation qualifying for the participations exemption are exempt from net wealth tax.

The domestic participation exemption regime has been modified with effect as of 1 January 2016 in order to comply with the amendments of July 2014 and January 2015 made to the EU Parent-Subsidiary Directive to introduce a general anti-abuse rule and an anti-hybrid rule.

The conditions that must be met to qualify for the exemptions are summarized below.

In some cases, tax treaties may provide for more favorable conditions.

Whether the exemptions apply to a particular set of circumstances must be determined on a case-by-case basis.

Enlightened by:

Wissam Mobayyed

Income tax exemption:

Tax exemption for dividends, capital gains and liquidation proceeds received – participation exemption.

Status of the Luxembourg beneficiary

Fully taxable resident collective entity listed in article 166 LITL paragraph 10; or

Fully taxable resident corporation not listen in article 166 LITL paragraph 10; or

Luxembourg permanent establishment of either: – a collective entity that is covered by the Parent-Subsidiary Directive; or – a corporation resident in a country with which Luxembourg has signed a tax treaty; or – a corporation or a co-operative company that is resident in an EEA country other than a member state of the European Union7.

Size of participation

The minimum participation that qualifies for the exemption is:

A 10% participation; or

An acquisition price of at least €1,200,00 to qualify for the dividend and liquidation proceeds exemption; or

An acquisition price of at least €6,000,000 to qualify for the capital gains exemption.

Status of the subsidiary

Collective entity listed and covered by the Parent-Subsidiary Directive; or

Fully taxable resident corporation not listed in article 166 LITL paragraph 10; or

Non-resident corporation fully subject to an income tax comparable to the Luxembourg corporate income tax. A minimum income tax rate of 9% generally satisfies this requirement as long as the taxable basis is determined according to rules and criteria similar to those applicable in Luxembourg.

The exemption also applies to participation held in a qualifying company through tax transparent entities.

However, decreases in the acquisition cost that result from dividend distributions are not tax deductible to the extent the dividends are tax exempt.

If a parent company writes off part or all of a loan to its subsidiary, the value adjustment is treated in the same way as any decrease in the acquisition cost of the participation, i.e. this write-off is taken into account when calculating the exempt capital gain portion.

Deduction of expenses

Expenses directly related to a participation that qualifies for the exemption (e.g. interest expenses) are only deductible to the extent that they exceed exempt income arising from the relevant participation in a given year. Decreases in the acquisition cost of a participation that qualifies for the exemption are deductible. The exempt amount of a capital gain realized on a qualifying participation is, however, reduced by the amount of any expenses related to the participation, including decreases in the acquisition cost, that have previously reduced the company’s Luxembourg taxable income.

Profit distributions falling within the scope of the Parent-Subsidiary Directive are not tax exempt in Luxembourg where the subsidiary is a collective entity listed and covered by the Parent-Subsidiary Directive (see first bullet point above under “Status of the subsidiary”), if

(1) such distributions are deductible by the payer located in another EU Member State (anti-hybrid rule) or if (2) the transaction is characterized as abusive within the meaning of the Parent-Subsidiary Directive (general anti-abuse rule). In this respect, a transaction may be considered as abusive if it is an arrangement, or a series of arrangements, that is not “genuine“ (i.e., that has not been put in place for valid commercial reasons reflecting economic reality) and has been put in place for the main purpose or one of the main purposes of obtaining a tax advantage that is not in line with the objective of Parent-Subsidiary Directive.

General anti-abuse rule and anti-hybrid rule